Prices are rising. Crude is up over 100% from November. Corn, soybeans, cotton and coffee are soaring, with gains approaching 50% or more. Gasoline costs roughly $1.02 per gallon more than last June – just in time for summer driving. Raw commodities tend to signal systematic inflation faster than finished goods. When it comes to inflation, we may be just getting started.

We expect the price of services to join the bull market in commodities soon. Services make up 70% of the American economy. More and more Americans are getting vaccinated and returning to restaurants, water parks and shopping malls. They are hopping on jets to see relatives and friends. Demand for services is rapidly expanding at the same time the labor to man these services is in short supply. Businesses, desperate for workers lost to the pandemic, are raising wages. “Transitory” or not, inflation is here, and it has momentum.

Volatility Makes Crypto-Currency an Iffy Inflation Play

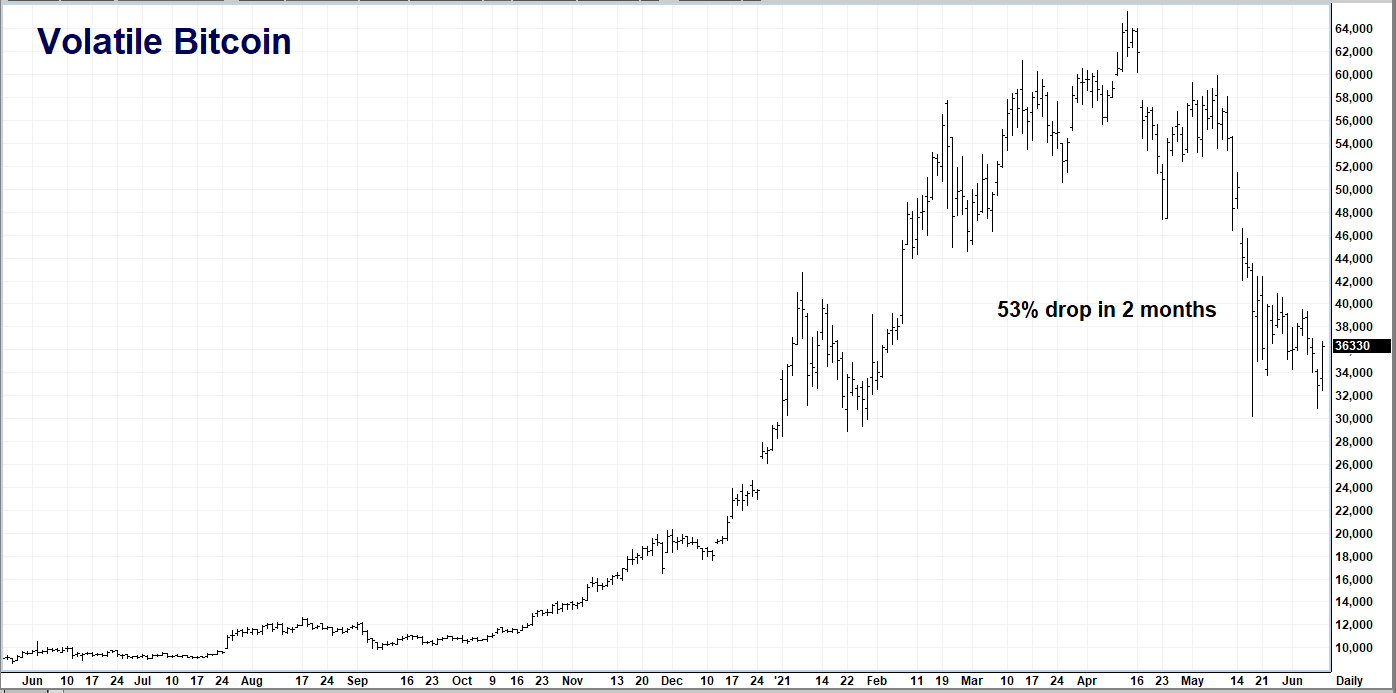

Bitcoin is considered an inflation hedge and store of value due to its guaranteed scarcity. Only 21 million Bitcoins will be minted. Electronic “mining” becomes harder and harder with each new coin produced, making fewer coins available over time. Bitcoin is also anonymous; holders do not have to identify themselves and can access their Bitcoin anywhere with an internet connection and the proper “key.” Bitcoin is much easier to transport and transfer than gold, and infinitely divisible. It is also much more volatile.

Investors who rushed to crypto-currencies (like Bitcoin) because of these characteristics are finding out digital money is not for the faint-hearted. As the chart below illustrates, Bitcoin initially soared on inflation fears and support from major financial influencers like Elon Musk. Bitcoin then gave back over half of its gains in just two months.

Data Source: FutureSource

Could Bitcoin turn on a dime and head higher? Sure. But it could also be in for more pain. Concerns about its climate-warming electrical usage, which caused former crypto cheerleader Elon Musk to reconsider his initial embrace, are beginning to have political ramifications. China is a preferred destination of Bitcoin miners due to its low cost of electricity. The Chinese government is now cracking down on miners who it considers to be abusing the system.

The US Government’s recovery of $2.3 million Bitcoin from the Colonial Pipeline hackers is another reason for concern. While we do not believe the blockchain was hacked per se – the US government could have worked with Colonial to insert code that made the transaction trackable or got the “key” from one of the hackers – the fact that it was tracked and recovered has damaged Bitcoin’s reputation for privacy. Bitcoin may be a paradise for traders comfortable with big swings in price, but its volatility leaves a bit to be desired when it’s used as a straight-up inflation hedge.

Gold Moved First and Appears Ready for Another Run

Good, old-fashioned gold sniffed out inflation well before cryptos, stocks or any other asset class. The proverbial “canary in a coal mine,” gold soared to new contract highs last August, well in advance of other commodities and far earlier than today’s concerning inflation data. We trusted gold’s prescience enough that we used these new highs then to predict the current bull market for commodities in general.

The weak dollar and artificially-low interest rates that sparked gold then are with us today. Trillions in stimulus money injected into the economy put cash directly into the pockets of consumers where it was spent on goods, driving up prices. We are fairly certain Congress will pass some form of infrastructure measure, likely with a price tag of $1 trillion, despite gridlock in Washington. Consequently, we don’t believe inflation will be going away any time soon.

Gold is on the march following a correction that took prices briefly below $1,700 per ounce. This correction corresponded with the explosion of Bitcoin to $64,000. Gold’s subsequent recovery also seems to match the timeline of Bitcoin’s recent collapse back to $32,000. Are these two markets in competition with one another for inflation hedge dollars? While their relative price movements bear watching, we’ll stick with gold for now.

Data Source: Reuters/Datastream

As the chart above illustrates, gold held long term support at $1,650 per ounce at the nadir of its correction earlier this year before rebounding nicely. The reopening of America, a weak dollar, and solid chart action could be setting the stage for an assault on old contract highs – and possibly much higher. Consequently, we are adding an additional upside target of $2,250 per ounce to the $2,050 target we set in our coin alternative blog post in April.

An Inflation Hedge That Won’t Break the Bank

Our $2,250 price target for December gold is 17.5% above Wednesday’s settlement price. This meshes nicely with the implied volatility of December at-the-money COMEX calls which clocked in yesterday at 14.3%. Our target is not far from what the market already expects.

RMB Group trading customers may want to consider buying December 2021 $2,150 gold calls while simultaneously selling an equal number of December 2021 $2,250 gold calls for $680 or less. We are looking for gold to hit our $2,250 upside target prior to option expiration on November 23, 2021. Your maximum risk is the net amount paid for the trade plus any transaction costs. This “bull call spread” has the potential to be worth as much as $10,000. Prices will change so contact your RMB Group professional for the latest.

Please be advised that you need a futures account to trade the markets in this post. The RMB Group has been helping our clientele trade futures and options since 1991. RMB Group brokers are familiar with the option strategies described in this report. Call us toll-free at 800-345-7026 or 312-373-4970 (direct) for more information and/or to open a trading account. Or visit our website at www.rmbgroup.com. Want to know more about trading futures and options? Download our FREE Report, the RMB Group “Short Course in Futures and Options.”

* * * * * * * *

The RMB Group

222 South Riverside Plaza, Suite 1200, Chicago, IL 60606

This material has been prepared by a sales or trading employee or agent of R.J. O’Brien & Associates (“RJO”)/RMB Group and is, or is in the nature of, a solicitation. This material is not a research report prepared by a Research Department. By accepting this communication, you agree that you are an experienced user of the futures markets, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions.

DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION.

The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from trades and statistical services and other sources that RJO/RMB believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades.