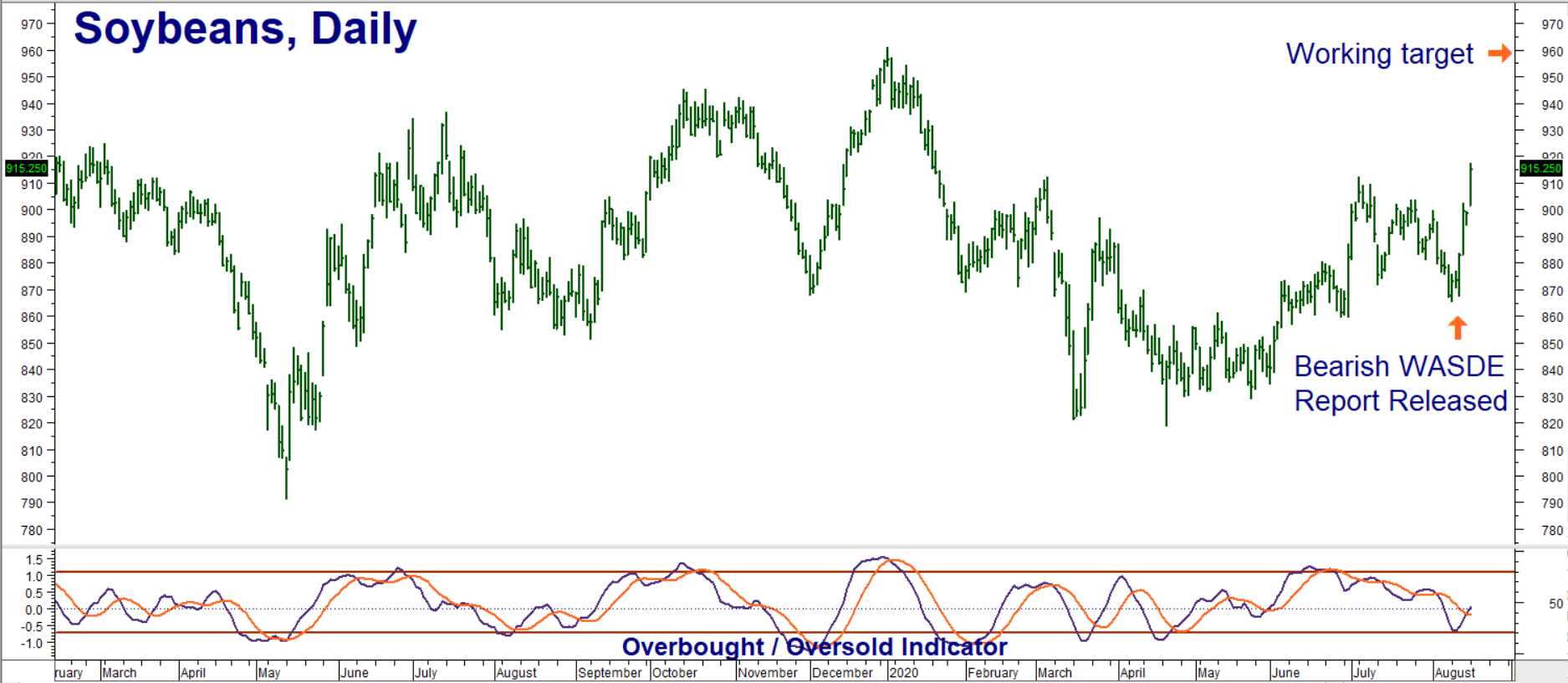

One of the most valuable signals of underlying change in a market is its reaction to news. A sharp decline following “bad news” can signal a scenario in which this bad news is already priced into the market. Soybeans soared following last week’s release of what would typically be an extremely bearish USDA world agricultural supply and demand (WASDE) report. Monday’s close over March’s $9.125 per bushel has finally turned sentiment positive.

Data Source: Reuters/Datastream

We believe soybeans’ ability to surge despite USDA estimates of higher stockpiles (and expectations of a new crop just short of a new record) is impressive. Not only was last week’s WASDE report bearish, it was downright depressing. We want to know why soybeans did so well because, if one believed the report, it certainly didn’t have a lot to do with supply and demand.

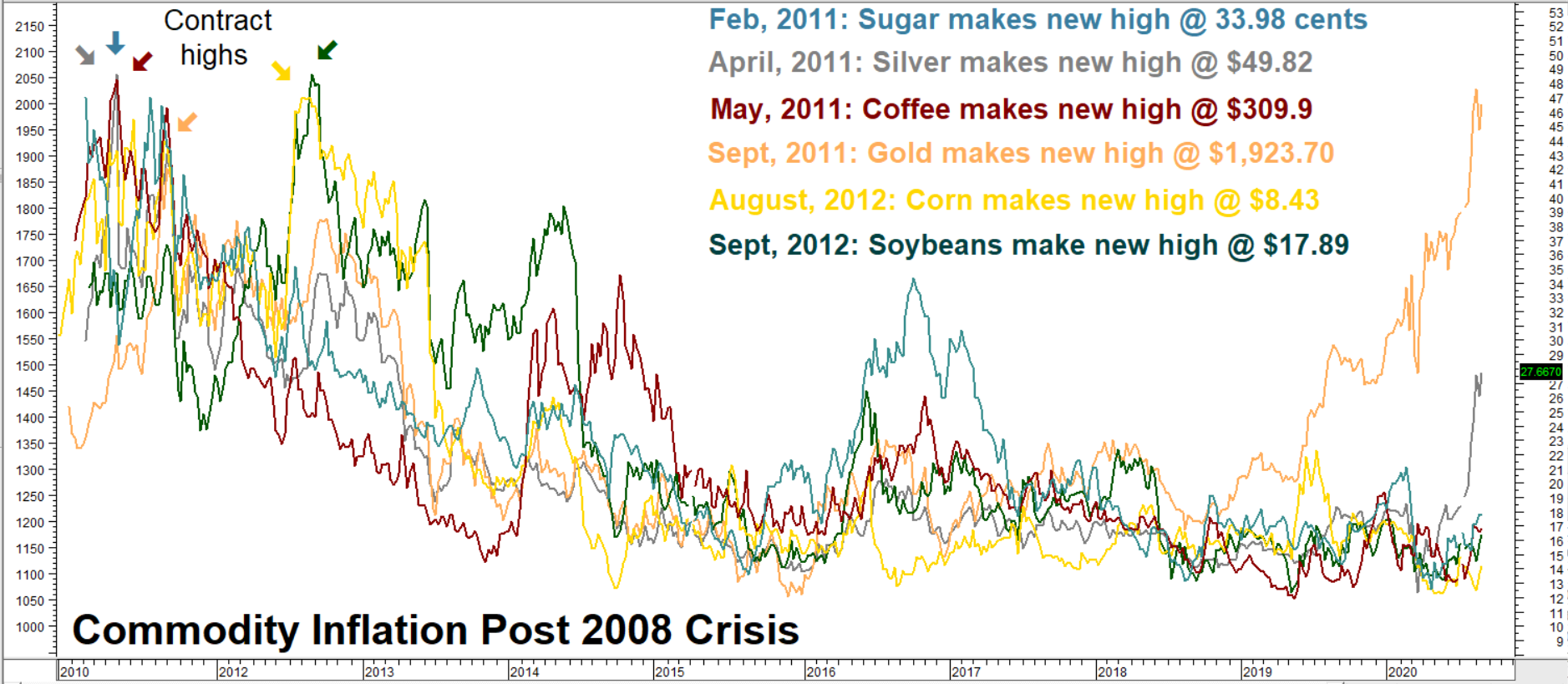

We took a look at what soybeans did during the last big commodity bull market, which occurred 3 years after the great recession of 2008/2009. Fueled by a weak dollar borne of artificially-low interest rates and months of aggressive Quantitative Easing (QE), commodities soared in 2011 and 2012, with many markets posting all-time highs that still stand.

Data Source: Reuters/Datastream

While supply and demand played a role in the 2012 soybean bull, it was the Fed’s weak dollar policies which set the stage for their ultimate explosiveness. As the chart above illustrates, sugar, silver, coffee, gold, corn (as well as other key commodities not on the chart) joined soybeans in making new contract highs. Even more powerful weak dollar policies today could result in a similar scenario for many of the same commodities.

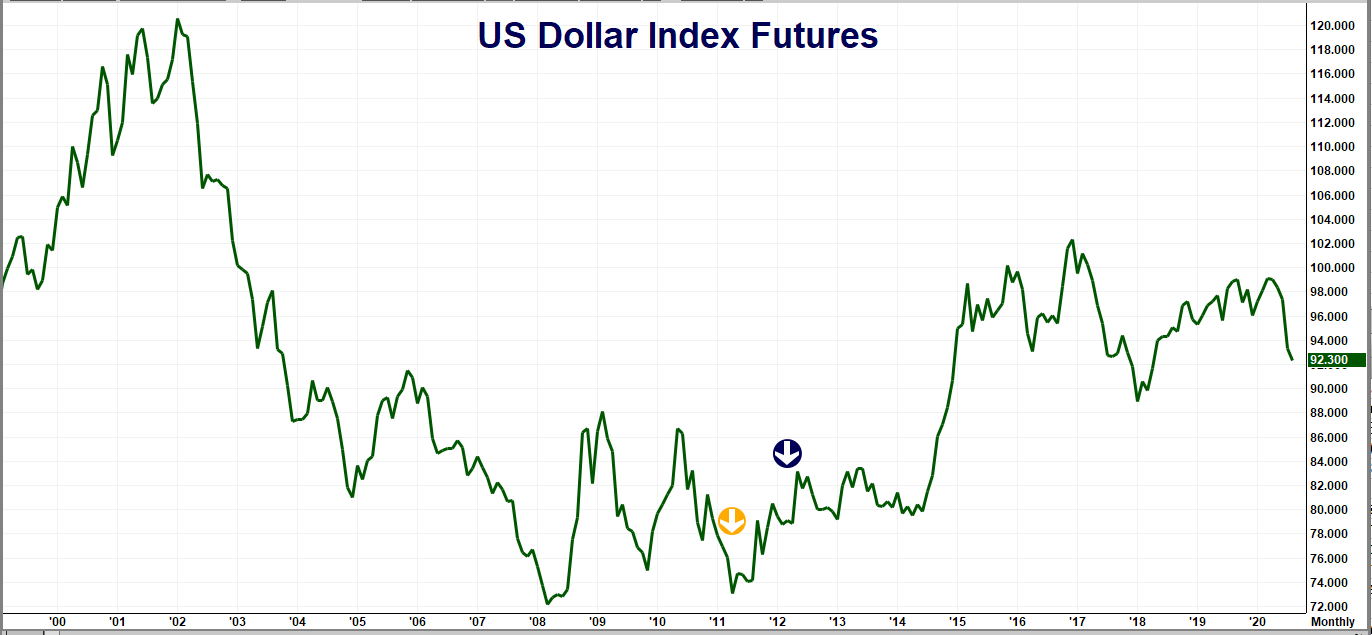

Commodities are priced in dollars. It takes more dollars to purchase an equivalent amount of any commodity when the greenback is weak. This is a key reason why the contract highs in all of the commodities shown in the “Commodity Inflation Post 2008” chart above correspond to a particularly weak period for the US dollar. (See chart below). The orange arrow corresponds to new contract highs in gold, silver, sugar and coffee. The blue arrow corresponds to contract highs in corn and soybeans.

Data Source: FutureSource

Gold is the only commodity to breach the contract high made during the last commodity bull market. The yellow metal is also the only commodity to serve as an alternative currency. Its rise in dollars is directly correlated with the current race to the bottom by the globe’s largest and most essential reserve currency. We expect other commodities will put on their rally caps and join gold and silver should the current drop in the battered buck continue.

Silver and gold are the strongest commodities on the board right now. And while we expect them to head much higher pre-election, neither is cheap anymore. RMB Group trading customers and those following our blog posts know we’ve been recommending long positions in both of these markets for the past few years. We will continue to do so, using corrections as buying opportunities.

Real “bargains” will need to be found elsewhere — in lagging agricultural markets like, sugar, corn, coffee and, yes, soybeans. Agricultural commodities could mimic metals and soar – especially if the current downward trickle of the dollar turns into a torrent, lifting all boats in the process.

Zero Interest Rates & Declining Dollar Poised to Power Commodity Bull

The trillions being thrown at the COVID crisis are many times the billions that followed the 2008/2009 recession. Create enough money out of thin air and you eventually get inflation. Unlike 2009, the Fed is determined to create and sustain it. The 2% inflation ceiling that governed Fed aspirations leading up to the last commodity bull market has now become a 2% inflation floor.

The Federal government is in on the party this time, injecting trillions of fiscal stimuli, unlike the 2008/2009 crisis. Much of today’s new cash is being put directly into the pockets of consumers and spent on actual goods and services instead of stock buybacks.

What will happen when the COVID crisis ends and months of pent-up consumer demand is unleashed on the economy? Prices will increase – some by a lot. We suspect commodities will be among the biggest beneficiaries of Fed and Federal largess, just as they were a decade ago. If we are right, gold will not be the only commodity to take out its old highs over the coming months and years.

Which brings us back to soybeans… Not only are beans the likely beneficiaries of expanding demand, they may also be on the radar of “smart money” investors looking for new inflation hedges. One of the reasons soybeans are rallying in the face of bearish news could be their attractiveness as a low-cost inflation hedge.

We can add other commodities to this list as well. Big rallies in metals, a historically expensive stock market, and the lack of reasonable yield from government paper is forcing big money to look elsewhere for opportunities. And why not? There are many commodities languishing in the bargain basement. We suspect they won’t remain cheap much longer.

(Editors’ Note: The Wall Street Journal ran a piece about this on Tuesday. Non-subscribers may run into a paywall.)

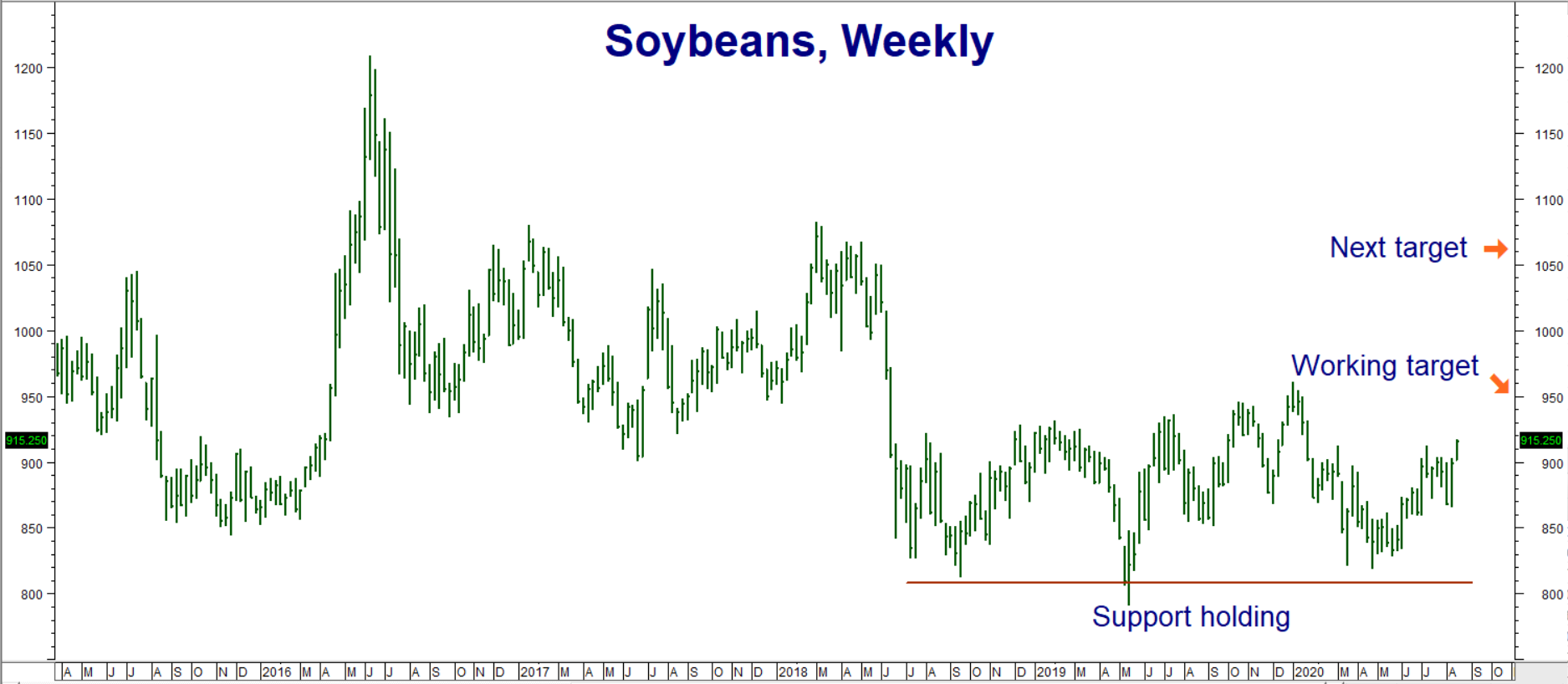

Soybeans Still Inexpensive

The current rally in beans is good news for RMB trading customers who took our early May suggestion to buy November $9.00 / $9.60 bull call spreads in soybeans. Our near-term target remains $9.60 per bushel. These spreads settled Monday for $1,045 each on Monday.

Soybeans and soybean options remain inexpensive – even after this surprising rally. As mentioned earlier, last week’s market action appears to be telling us the worst is already been priced in. If we are right and the weak dollar continues to be a driving force in commodities, soybeans should have a lot more room to the upside.

Data Source: Reuters/Datastream

RMB Group trading customers may want to consider establishing or adding to existing positions by purchasing July 2021 $9.80 / $10.60 bull call spreads for $675 or less. Look for the July 2021 futures contract to hit our new $10.60 per bushel target prior to the expiration of July 2021 options on June 25, 2021. Your maximum risk is the amount you pay for your spreads plus transaction cost.

These bull spreads have the potential to be worth as much as $4,000, although we expect to exit them beforehand. Prices can and will change so contact your RMB Group broker for the latest, and ask about current opportunities in other agricultural commodities like sugar, coffee and corn. We’ll take a good look at the yellow grain and review outstanding long positions in sugar and natural gas in future blog posts.

Please be advised that you need a futures account to trade the markets in this post. The RMB Group has been helping our clientele trade futures and options since 1991. RMB Group brokers are familiar with the option strategies described in this report. Call us toll-free at 800-345-7026 or 312-373-4970 (direct) for more information and/or to open a trading account. Or visit our website at www.rmbgroup.com. Want to know more about trading futures and options? Download our FREE Report, the RMB Group “Short Course in Futures and Options.”

* * * * * * * *

The RMB Group

222 South Riverside Plaza, Suite 1200, Chicago, IL 60606

This material has been prepared by a sales or trading employee or agent of R.J. O’Brien & Associates (“RJO”)/RMB Group and is, or is in the nature of, a solicitation. This material is not a research report prepared by a Research Department. By accepting this communication, you agree that you are an experienced user of the futures markets, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions.

DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION.

The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from trades and statistical services and other sources that RJO/RMB believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades.