When the world’s largest exporter of soybeans wants to import them, it’s time to sit up and take notice. Population-heavy China is in a hurry to rebuild a domestic hog herd decimated by African Swine Fever. Feeding these piglets requires grain and oil seeds. The trade war with the US caused the Chinese to turn to Brazil – the world’s biggest producer and exporter of soybeans – for “beans”, stretching Brazil’s domestic stockpile to its breaking point. This forced Brazil to lift all tariffs on imported soybeans.

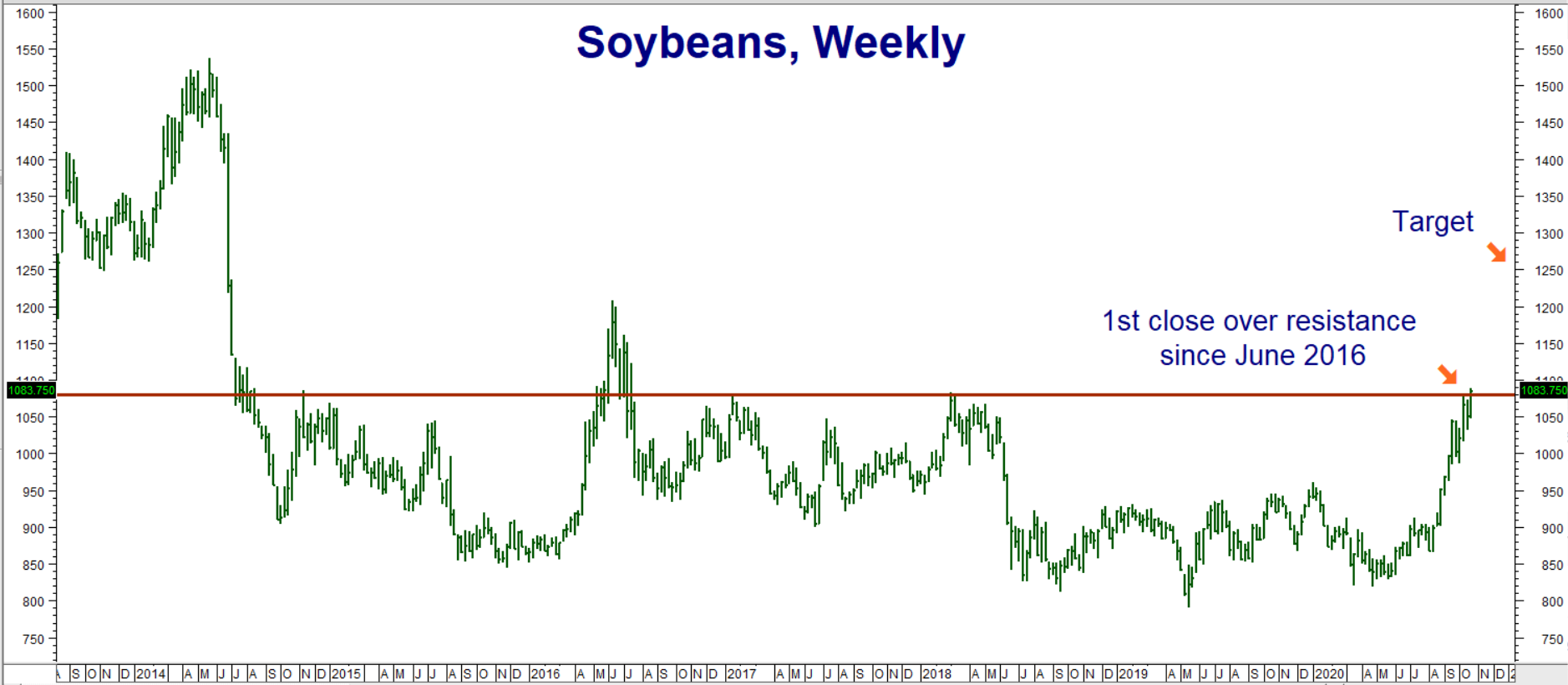

With Brazil unable to meet demand and China’s appetite for beans growing (see chart below), the Middle Kingdom has returned to North America for its soybean needs, powering prices higher. Front month soybean futures have risen 30.5% from their March 17th COVID lows of $8.22 per bushel to $10.7375 as we write this. We expect this rally to continue for at least 6 to 8 months – and maybe even longer.

China Not the Only Driver of Soybean Bull Market

China is not the only driver. Nearly half of the continental United States is experiencing some form of drought. Dry conditions in the critical month of August caused soybeans harvested in dry areas to take on a smaller size, reducing the nutritional value of each affected plant. Size matters in soybeans.

Dry conditions in South America have delayed planting there, squeezing an already-tight global supply / demand balance even further. Argentina is a major supplier of soybeans. A collapse in the Argentine peso – typically bearish for soybeans – is not benefiting farmers who are forced to accept the “official” exchange rate of 54 pesos per dollar for their beans. (The black-market rate is currently 167 per dollar – 3 times this amount.) An additional 30% tax on soybean exports shrinks the incentive for Argentinian bean farmers to produce.

Demand for soybeans is not only growing in China. Global population has grown 28% since the turn of the century while demand for soybeans has doubled. Rising standards of living have changed global diet patterns to favor meat, which is basically grain in another, less efficient package. It takes roughly 4.1 pounds of grain to produce one pound of pork and 7 pounds of grain to produce one pound of beef. As the chart below illustrates, the global demand for soybeans shows no indication of slowing any time soon.

Goldman Sachs Calls for Bull Market in Commodities

We’ve been calling for the same thing for over a year. It’s nice to have a big-name company join us. Like RMB Group, Goldman is focusing on non-energy agricultural commodities and metals. Goldman lists four major reasons behind their call: 1) Chinese demand, 2) adverse weather, 3) dollar weakness, and 4) higher inflation due to an uber-easy Federal Reserve and the potential for more government stimulus on top of the trillions injected by the CAREs Act.

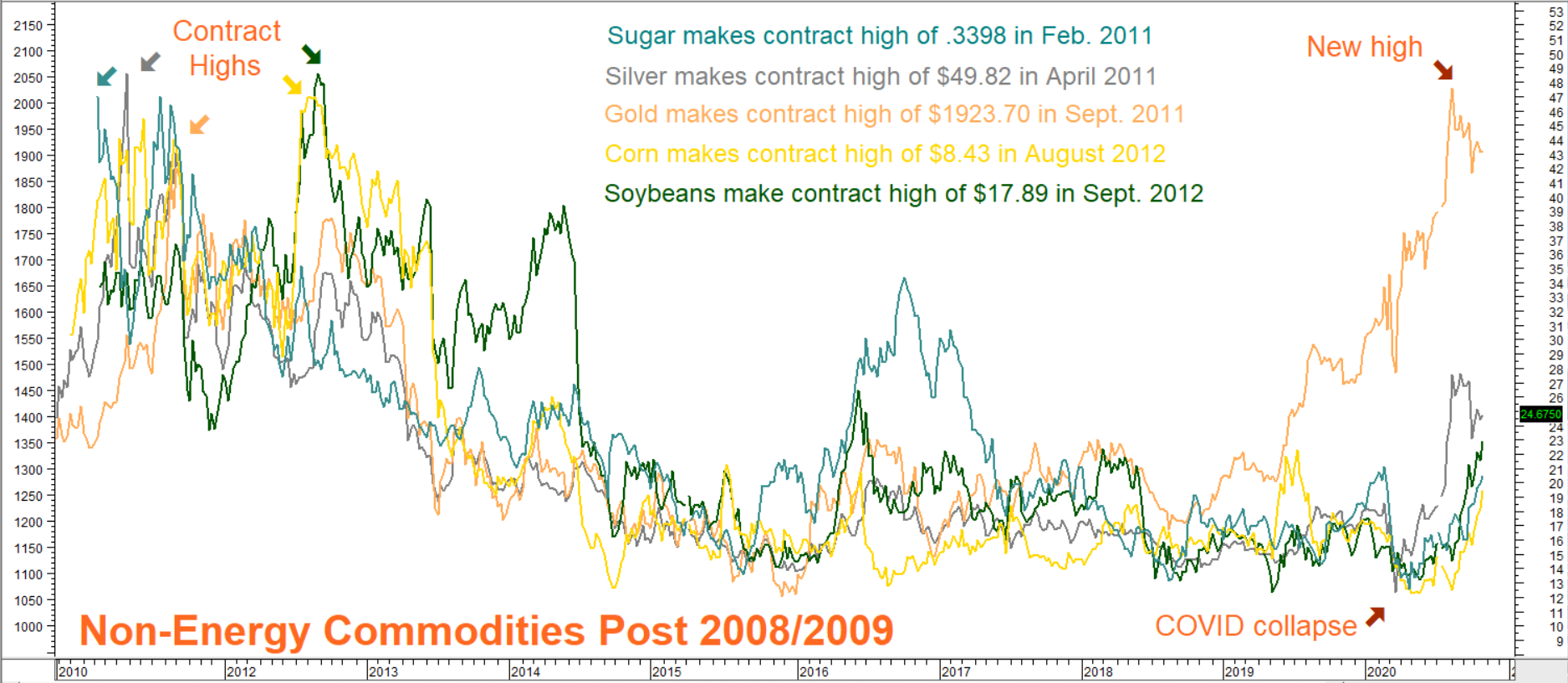

The chart below shows what happened to some key non-energy commodities after the Great Recession of 2008/2009. Many commodities made new all-time highs following the Great Recession, most driven by the same forces present now. The only real difference is the amount of government stimulus being thrown at COVID. The Feds spent less than a trillion dollars to combat the 2009 Housing Crisis. They have already spent $2 trillion in the age of coronavirus. We expect trillions more to follow.

Silver and sugar led the commodity charge last time. Gold is the hands-down leader now. Gold is a financial metal, so we expect it to react faster to the highly inflationary Monetary and Fiscal tools being used to fight the economic damage caused by COVID-19. Gold is the only major commodity to make a new contract high in the current environment. We suspect it won’t be the last.

Data Source: Reuters/Datastream

All the other non-energy commodities on the chart above appear to have negated their nearly decade-old bear markets. They could have a lot more room to run – especially if the drought conditions which marked the years after the 2008/2009 recession repeat. Weather is notoriously fickle, but Mother Nature appears to be sticking to the script so far. A continuation of this year’s dry conditions would be very bullish for soybeans in particular, causing them to outperform a potentially choppy stock market over the next 6 months.

Early Innings for Soybean Bull?

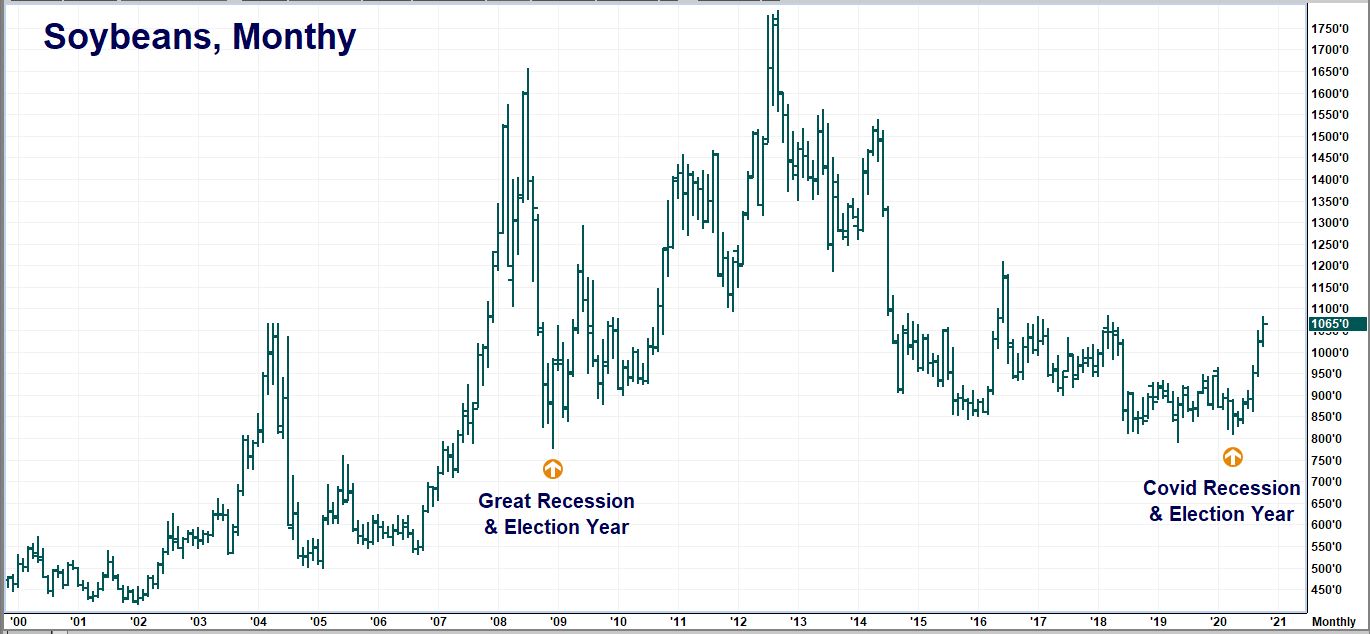

The two most recent recession cycles appear to have lined up with American presidential elections. The 2008 Housing Crises which marked the end of the final George W. Bush presidential term caused massive government intervention. This helped fuel a smoking hot bull market in commodities. The stimulus being used to fight the COVID crisis at the end of Donald Trump’s first presidential term is already three times larger. Commodities, including soybeans, have responded accordingly.

Soybean futures rallied robustly following the housing-led election-year recession of 2008. Helped by drier-than-normal conditions, beans stayed in the teens through most of the first term of Barack Obama before topping out at $17.89 per bushel in September 2012. History may not repeat, but it appears to be rhyming. Soybeans rose for three years following the Great Recession. We believe “beans” could be in the early innings of a multi-month, and perhaps multi-year, rally. Weather will determine how high prices will climb.

Data Source: FutureSource

“Backwardation” is Bullish for Beans

Most agricultural commodity futures contracts exhibit a condition called “contango” most of the time. Back month contracts tend to trade at higher prices than front month contracts to account for storage costs and lost income. It costs money to store soybeans. It also costs lost opportunity.

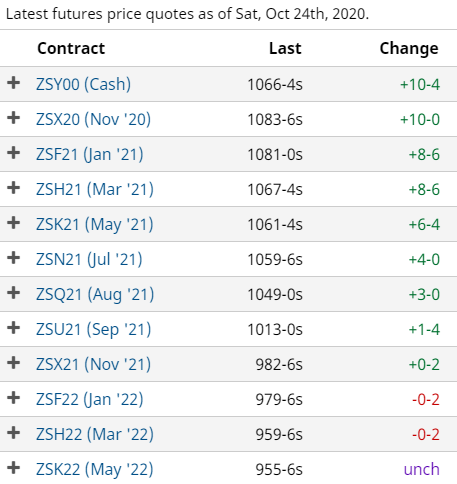

Forgoing a cash sale to store soybeans leaves a farmer with less money to spend preparing for next year’s crop and/or invest in other instruments. Potential buyers of soybeans looking to lock in a future price often buy back month futures contracts instead of front month or cash contracts which would force them to accept delivery and store the product until it is used. These “carrying costs” are generally priced into back month futures contracts, making them more expensive than front month contracts closer to delivery. The table below illustrates a classic contango market in Coffee. It shows how normal carrying charges cause back month prices to rise. (Note “Cash” entry is not a futures contract.)

Coffee in Contango

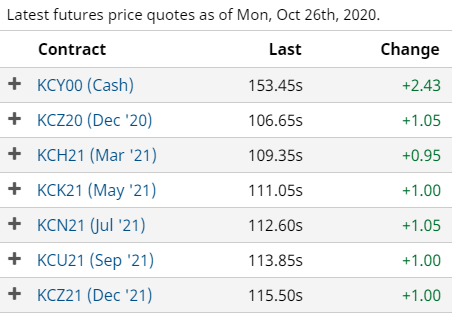

“Backwardation” is the opposite of “contango.” In “backwarded” markets, front month futures contracts are more expensive than back month contracts. This typically happens during supply shortages. End users, desperate for product, focus their buying on front month futures intent on taking actual delivery. Prices rise as other users pile into the market forcing short sellers to “cover” (buy-back) their positions as well. Backwardation is generally a very bullish signal. The table below shows soybean futures contracts backwarded out as far as May 2022.

Backwardation tends to last as long as the market believes shortages will last. It also has advantages for longer-term bullish traders. Normal “contango” markets are biased against bullish traders because deferred contracts are more expensive. Long-term holders have to “roll” their position into deferred contracts to maintain their exposure and avoid delivery, paying a premium for each roll. It’s the reason why the returns of many commodity-specific ETFs often lag the returns of the actual commodity.

The lower price of deferred contracts in a backwarded market tend to favor bulls who wind up paying less when rolling their positions into deferred-month contracts. November soybean futures are known as “new crop” contracts because their delivery period corresponds with the North American harvest. July soybean futures are known as “old crop” contracts because their delivery period falls between the North and South American harvests. The price of “new crop” November 2020 futures is $10.8575 per bushel in the table below. The price of the July 2021 futures is $10.5975 – 26 cents per bushel less.

Backward Beans

Carrying charges are negative, giving bulls a potential advantage should tight market conditions extend past South America’s 2021 harvest. The market is pricing a tight but workable supply/demand scenario now. July 2021 futures could move much higher if current shortages grow larger and/or the adverse weather conditions delaying planting in South America continue.

Playing the Long Game in Soybeans

RMB trading customers who followed our research know that we have been bullish soybeans since the precipitous, albeit brief, COVID collapse back in March. The market hit our first objective of $9.60 per bushel on time, but shattered our second objective of $10.60 per bushel much sooner than expected. Soybeans are overbought, so waiting for a big correction would normally be our “go to” move.

However, Brazil’s decision to remove tariffs on soybean imports is causing us to rethink this approach. It tells us that underlying fundamentals could be a lot tighter than the latest USDA figures indicate. Backwardation in the futures market seems to confirm this. We don’t want to be out of this market too much longer – especially given recent price action. Will we get a correction? Probably. But we believe it will be smaller and more short-lived than we originally calculated.

Data Source: Reuters/Datastream

July bull spreads give us a way to re-enter this market without exposing ourselves to excessive risk. They keep us long during the typically seasonally-friendly late spring / early summer period. RMB Group trading customers may want to consider re-entering this market on the long side by placing an order to buy July 2021 $11.60 soybean calls while simultaneously selling an equal number of July 2021 $12.60 soybean calls for a net cost of $800 or less.

Your risk is the net amount paid for your spreads plus transaction costs. Each spread has the potential to be worth as much as $5,000. Consider exiting half of your spreads if and when their value doubles from your initial fill price. Exit the remainder if and when our $12.60 per bushel target is hit. July 2021 soybean options expire on June 25, 2021.

Please be advised that you need a futures account to trade the markets in this post. The RMB Group has been helping our clientele trade futures and options since 1991. RMB Group brokers are familiar with the option strategies described in this report. Call us toll-free at 800-345-7026 or 312-373-4970 (direct) for more information and/or to open a trading account. Or visit our website at www.rmbgroup.com. Want to know more about trading futures and options? Download our FREE Report, the RMB Group “Short Course in Futures and Options.”

* * * * * * * *

The RMB Group

222 South Riverside Plaza, Suite 1200, Chicago, IL 60606

This material has been prepared by a sales or trading employee or agent of R.J. O’Brien & Associates (“RJO”)/RMB Group and is, or is in the nature of, a solicitation. This material is not a research report prepared by a Research Department. By accepting this communication, you agree that you are an experienced user of the futures markets, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions.

DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION.

The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from trades and statistical services and other sources that RJO/RMB believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades.