These are critical times. The post-Cold-War era of cooperation that has provided much of the globe’s prosperity since the fall of the Berlin Wall is ending. What will replace it is currently being hashed out by political and economic changes that are currently sweeping the globe. Brexit in the UK, Trump in the US, Xi in China, Bolsonaro in Brazil, and the rise of Hindu nationalism in India are manifestations of the growing discontent with the status quo.

Perhaps most disturbing is the “mother of all trade wars” currently being waged the world’s two largest economies – China and the US. This war will have far-reaching consequences – none of which, in our opinion, will be positive. History tells us that trade wars are never good for anybody. Trade wars lead to economic depression like the Smoot-Hawley Tariff Act did in the early 1930s US or to other economic dislocations that upend social structure and increase tension between trading partners. There is no reason to expect the outcome to be different now.

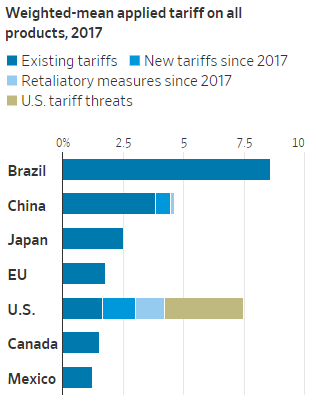

China and the US are the main players in today’s trade war, but as the chart (source: Deutschbank) suggests, they are not the only ones firing the cannons. However, it is the US that has become the aggressor, dramatically increasing both new tariffs and tariff threats since 2017. Many of these tariffs and threats are not aimed at China at all but rather at American allies like Canada, Mexico and the EU. This is not a bullish development – especially for growth. Since stocks thrive on growth, it is certainly not a bullish development for them either.

The quote below is from an August 18 article in the Wall Street Journal. The entire article deserves a read. (Note: non-subscribers may be blocked by WSJ’s paywall.)

“Most economists say restricting trade imposes costs on businesses, consumers and the wider economy. UBS calculates the blossoming trade conflict has kept the U.S. economy around 0.75% smaller than it would have been had tariffs stayed where they were.

“Global output has also taken a hit: UBS says the world economy is around 0.4% smaller than it otherwise would have been. The damage will rise to 0.7% if Mr. Trump pulls the trigger on all threatened tariffs.

“The International Monetary Fund recently cited trade tensions as the prime reason it lowered its global 2019 growth forecast to 3.2% from its April projection of 3.3%. The world economy expanded 3.6% last year.”

Balkanization Will Be Costly

Another article that caught our attention was a “Seeking Alpha” post by William Tidwell. Although Mr. Tidwell is writing about memory chips, we believe his observations are applicable to many other markets, including commodities. Here are some of his observations:

- The global trend towards greater balkanization will continue as the world gets split into two “warring economic camps.”

- The trade war between China and the US is unresolvable given their divergent agendas. There is no “win-win” scenario possible. This makes the probable outcome potentially very costly.

- World GDP growth will be reduced, and perhaps go negative for a while before a new equilibrium is established.

- Manufacturing costs will be higher until adaptive assembly line robotics becomes a cost-effective alternative to humans.

- Productivity growth will be reduced and may even go negative, at least for the first few years.

- Countries will experience high levels of political and social stress – with some countries potentially subjected to serious damage.

- Geo-political flash-points will increase, and military tensions will rise, potentially to a 1960’s-like Cold War level.

No matter what their political leanings, we believe nearly everyone will agree that burgeoning US-China trade war is disruptive. Part of the reason why Donald Trump was elected President was because people who felt left behind by the global economy wanted a president who would be disruptive. To them, Trump is simply fulfilling a campaign promise. This desire for disruption is not limited to the US. It is global.

Change can be good but it can also have unintended consequences. Big, out-of-control economic accidents are often the root of violent conflict. Global shooting wars usually start when big powers attempt to regain by force what they’ve lost due to trade wars and/or other economic dislocations brought about by bad decisions.

The global economic slowdown caused by the Great Depression in the 1930s, America’s embargo of the sale of oil to Japan in the early 1940s, and the rise of the Nazi Party in Germany were all key catalysts of World War II. Roosevelt’s embargo of oil to Japan was largely responsible for the Japanese attack on Pearl Harbor. The rise of the Nazis in Germany doesn’t happen without the 1920s hyperinflation of the Weimar era.

We are not predicting another World War but we do expect political and economic tensions to continue to increase to ever more dangerous levels. That means more volatility as the forces driving economic Balkanization continue to be mirrored politically.

It is now “us-versus-them” virtually everywhere, triggering all of our species’ primitive, tribal impulses in the process. These impulses, once necessary for survival, are dangerous in today’s interconnected world. Consequently, we are fairly certain the coming transition will not be a smooth one.

Gold: A Shelter from the Storm

Mix uncertainty with volatility and you get a recipe for huge gains or crushing losses. That’s why we will continue to focus on option strategies that have a fixed, easily identifiable risk. Gold and its other cousins in the precious metals sector tend to do well in a turbulent macro-economic environment. This is why the majority of our blog posts in 2019 have dealt with precious metals.

Data Source: Reuters/Datastream

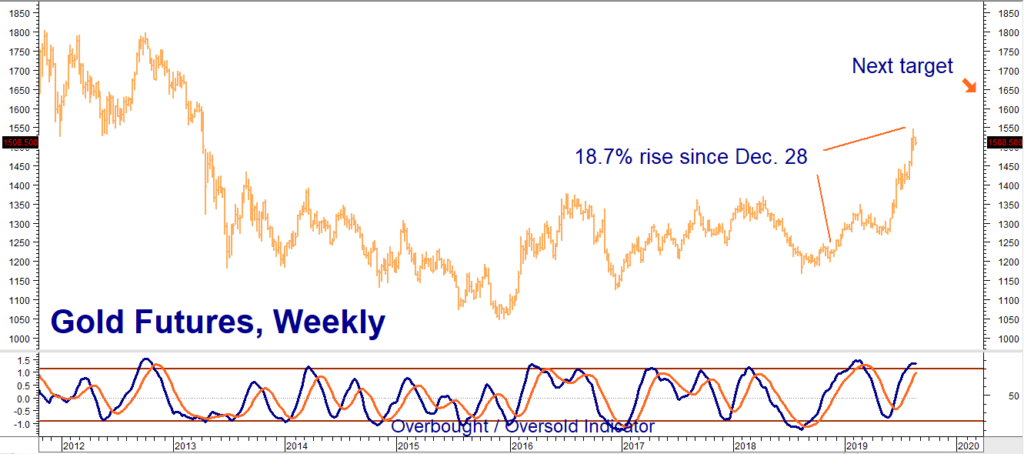

Gold and silver have thousands of years of history as alternative currencies and stores of value. Gold is up 18.7% since December 2018, meeting two of our three upside targets in the process. That it has risen in nearly every currency and has been able to post these gains despite the strong dollar indicates how strong it is. Investors and central bankers are buying it both as an alternative currency play and as a hedge against global chaos.

As the chart above illustrates, gold is becoming overbought. While this doesn’t mean it cannot go higher, investors looking to make investments in the precious metals sector now may want to consider long positions in silver instead. Silver is extremely cheap in relation to its richer cousin and has a lot of catching up to do. A continuation of the bull market in gold could spur an even bigger move in silver.

Investors Should Tread Cautiously In Stocks

Gold and silver may thrive on chaos but stocks do not. The same uncertainty and fear that powers bull markets in the metals can do the exact opposite to stocks. Stock investors betting on lower interest rates from the Fed and a reasonable resolution of the Sino-US trade war have kept the market stable. They may get neither.

When it comes to the trade war, Donald Trump is playing a short term game. He needs a satisfying resolution prior to the 2020 general election, which gives him about 6-months at most. Stock investors are counting on this. They expect Trump to cave, resulting some kind of agreement, even if it isn’t the deal everyone is looking for. Business is fleeing China and will probably not return. But higher costs mean this business is not coming back to the US either.

A trade deal will probably give the stock a short-term boost. However, we don’t believe it will matter over the long haul; the damage has already been done. Tariffs have already thrown sand in the gears of global commerce. The machinery hasn’t stopped running yet but global growth is decelerating, along with the economies of China, the US and the EU. We believe that nothing agreed to over the next six months is going to reverse this trend.

Stock market investors tend to be an optimistic lot. They also have a tendency to change their collective tune on a dime. The bull market in stocks is now the longest in history. The “easy money” has already been made. We don’t know what trigger event will cause stock market investors to cut and run this time but, with values so extended, we suspect it won’t take much.

China’s “Nuclear Option” and the Bond Market

China is playing the “long game” and can afford to be patient and strategic. It definitely has the most to lose, but its political system means President Xi has a far greater ability to weather the economic carnage war than any American President.

China is also one of the biggest holders of US Government bonds and notes. The bond market is far larger than the stock market. This means disruptions in the former can be more economically damaging. Fear that the Chinese would invoke the “nuclear option” and dump all of its US Treasury debt has been around for years. But that is not what is happening – at least not yet.

It turns out that China has been busy shedding American Treasury paper since the start of the tariff war in 2017, but has been doing so gradually. Instead of falling, bond prices have been soaring as bond yields have fallen – the exact opposite of what many were expecting. Negative interest rates in Europe have had a far greater effect on the US Treasury market than the Chinese.

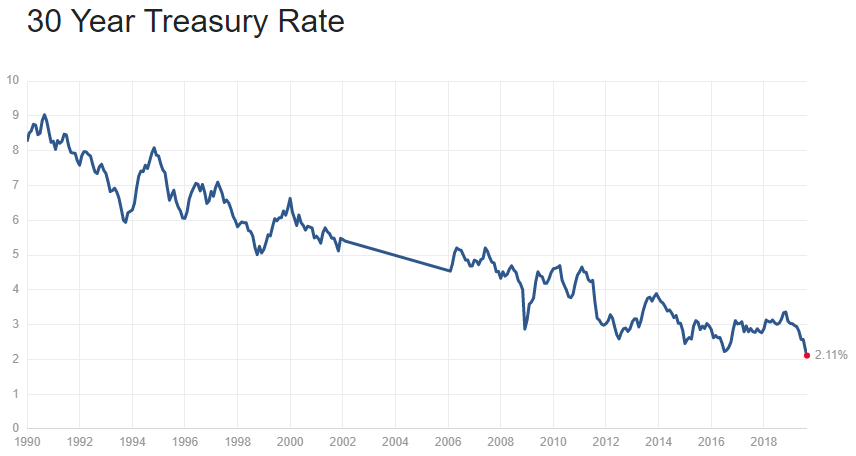

Source:Multpl.com

The yield on the 30-year bond just made an all-time low — lower than during the great recession of 2007/2008. Negative interest rates in Europe mean investors are literally paying governments and banks to hold their money. Instead of locking in guaranteed losses, they are turning to the US Treasury market, inflating prices and depressing yields to unnatural levels in the process.

Analysts are using artificially depressed US Treasury yields as a signal of coming recession. This changes market psychology which, ironically enough, could turn far enough south to actually cause the recession the analysts say they these lower rates are signaling. The tail could be wagging the dog.

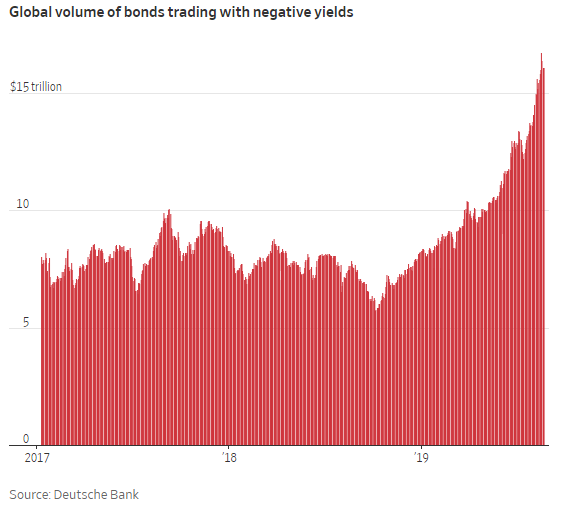

Germany which, like the US, has a slowing but growing economy just auctioned its first bund offering with negative interest rates, increasing the amount of outstanding global government debt with negative yields to almost incomprehensible levels. We believe there is a practical limit to the current negative interest rate madness. It is economic sophistry of a special order.

The only reason one would buy any debt instrument at a negative yield is the expectation that they will eventually able to sell that debt for a higher price in the future. We believe this is ultimately a formula for global economic disaster. Prices will eventually start going down. Millions of investors will be unable to exit their positions in time. Trillions could lost. No wonder gold is doing so well.

We believe the best play in bonds could be a contrary one – especially with virtually everyone leaning on the lower rate side of the boat. We haven’t pulled the trigger yet, but may do so shortly. We’ll have more on the insane global bond markets in future posts.

Alternative Assets & Professional Management Could Be Key to Surviving Turbulent Times

With both stocks and bonds overextended after decade-long bull markets, political and economic uncertainty on the rise and the odds of an economic accident seemingly growing by the day, now may be the time to take a look at alternative asset classes. Gold has been one of the alternative markets we’ve been focused on, but it is fairly well along. We still recommend holding long positions in the yellow metal but, as we mentioned earlier, we like silver better for new positions.

We also believe big opportunities still exist in the beaten down agricultural sector and will be monitoring these markets for low risk option plays as the rest of 2019 unfolds. Our individual trading customers should watch this space.

This could also be the perfect time to consider adding professionally managed futures accounts to one’s asset mix. Futures money managers (known as Commodity Trading Advisors or “CTAs”) have can go both long and short, giving them the ability to capitalize on bull and bear moves in any market. Managed futures accounts have a multi-year tendency to “zig” when stocks and bonds “zag,” making them an excellent diversification tool.

Many CTAs specialize in certain asset classes like, agriculture, precious metals, currencies, interest rates and energies. Others trade a broad portfolio of different markets. They all must supply “Disclosure Documents” — which include audited track records — to prospective customers. Download our Free Report, “Opportunities Outside the Stock Market” to learn more about how professionally managed futures accounts can help you survive the coming storm.

Please be advised that you need a futures account to trade the markets in this post. The RMB Group has been helping its clientele trade futures and options since 1991 and are very familiar with all kinds of option strategies. Call us toll-free at 800-345-7026 or 312-373-4970 (direct) for more information and/or to open a trading account. Or visit our website at www.rmbgroup.com.

* * * * * * * *

The RMB Group

222 South Riverside Plaza, Suite 1200, Chicago, IL 60606

This material has been prepared by a sales or trading employee or agent of R.J. O’Brien & Associates (“RJO”)/RMB Group and is, or is in the nature of, a solicitation. This material is not a research report prepared by a Research Department. By accepting this communication, you agree that you are an experienced user of the futures markets, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions.

DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION.

The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from trades and statistical services and other sources that RJO/RMB believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades.