There has been a lot of talk in the financial press about the shape of the COVID-19 recovery. “V” shapers view the huge 38% rally in the S&P 500 as predictive and a solid signal of a quick snapback. “W” shapers think stocks have gotten ahead of themselves and will re-test lows before recovering. “U” shapers believe the recovery will be slower, and that stocks will trade sideways until finally breaking out to the upside sometime in 2021. Virtually no one is predicting new lows, and virtually everyone expects an imminent recovery.

The prophecies of doom and gloom that accompanied the mid-March COVID-19 crash have vanished. They have been vanquished by the Federal Reserve’s promise to do “whatever it takes” to support financial markets – all financial markets. The Fed is now buyer of first resort, last resort and every other resort in-between. The “Fed put” that created a floor under stocks following the 2008/2009 recession has morphed into an “everything” put, creating floors under everything.

“Don’t fight the Fed,” once a favorite saying of stock market traders, has taken on a whole new meaning. Investors are not only snapping up stocks, they are gorging themselves on corporate debt, junk debt and municipal debt, confident that Jerome Powell and Company will be there for them should things hit another rough patch. Combine the Fed’s “everything” put with FOMO (fear of missing out) and you get the rocket ride we are currently experiencing. It is this, not some alphabetical market prediction, which is powering stocks right now.

When the Fed lowered interest rates to zero, they made it impossible for savers to get ahead, forcing them into risk assets like stocks. The recent introduction of commission-free trading and millions of newly-minted Mom and Pop traders quarantined at home and confident the Fed has their backs have turned the stock market into a giant casino whose patrons are on a winning streak. The only losers are those not playing the game. FOMO is causing these newcomers to forget another popular adage: “The house always wins.”

Stocks are Expensive

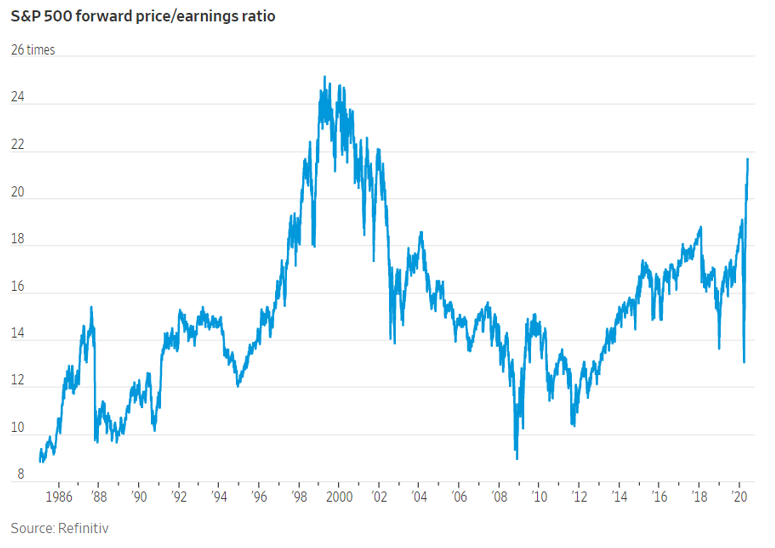

COVID-19 is expected to reduce overall stock market earnings by about 20%, giving the S&P 500 a forward PE of 21.6. This is 24% higher than the market’s 17.4 forward PE the last time stocks were at these prices in October 2019. A bigger-than-expected decline in earnings will increase the market’s forward PE even more, rendering it even more expensive. Re-openings across all 50 states, along with the nationwide demonstrations roiling the US, are creating conditions favorable to new coronavirus outbreaks. This could put a big damper on any recovery.

The Fed’s Monster

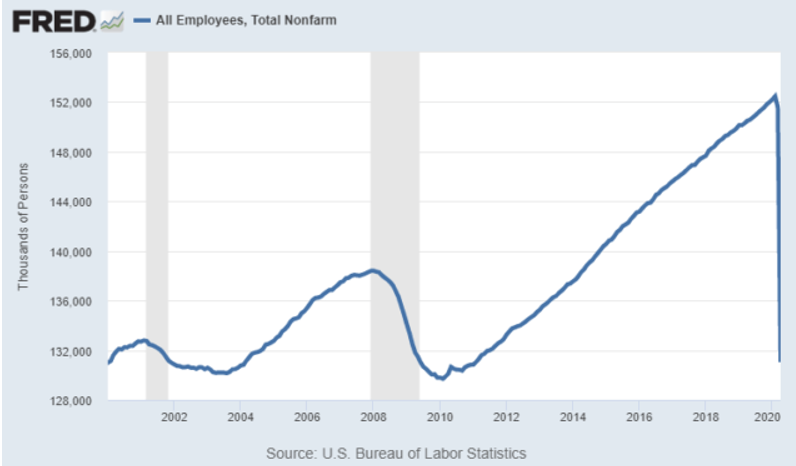

The Fed’s “everything” put did its job. It stopped the March meltdown that threatened to crash the economy. But by doing so, the Fed unwittingly created a monster. Like its remedy for the 2008/2009 crash, the current intervention has disproportionally favored the richest Americans at a time when US unemployment could rise as high as 20%. A 20% unemployment rate not only means a fifth of the nation will be without an income; it will also leave the bulk of this group without healthcare.

Income inequality has played a big role in the political civil war raging in the US since the last recession. It was a big factor in Donald Trump’s election. Nearly half of Americans don’t own stock. Rising stock markets do nothing for them. The richest 10% of Americans own 84% of stocks. The current rally is not helping most of the 20 million people who lost their jobs in April or the millions more in May.

The Fed was created to protect the banking system. It does not have the tools to address the economic and social issues exacerbated by the C-19 virus. Its solutions bypass the typical American. The Fed’s “everything” put is working like a charm, but it is definitely not working for everybody.

The Fed’s stock market put didn’t work for the common man during the 2008/2009 recession either. Banks got bailed out, but Main Street didn’t. “Occupy Wall Street” protests sprung up everywhere. It took years for the Fed’s actions to directly impact the well-being of most Americans. By that time, people were soured on the whole system and frustrated enough to dump the party in power.

November Election Not Discounted by Current Prices

Today’s stock market gains may be generating the same kind of resentment. They could backfire over the long term, increasing the odds of another leg down as we approach the election. The positive effects of today’s rising stock market will not be experienced by most Americans for years – certainly not in time for November 3rd. People are angry. Angry people vote. There is a growing possibility that the party currently in power could not only lose the Presidency, but also the Senate, threatening many of the stock-friendly policies currently in place.

Huge deficits resulting from the 2017 Tax Cut, COVID-19 bailouts, and any new initiatives such as an infrastructure bill, will require huge amounts of new tax revenue. Democrats have made no secret of where these funds will come from if they win. Stock prices are currently discounting none of the potential revenue-generating possibilities below:

- Repeal of the 2017 corporate tax cut.

- Termination of favored tax treatment of qualified dividends.

- Termination of favored tax treatment for long-term capital gains.

- Requirement of a minimum tax for all companies.

- Tax on stock transactions themselves.

- Higher income taxes on the wealthy.

Nobody knows what is going to happen on November 3. However, the market will eventually have to discount the possibility that at least some of the items listed above will come to pass if current polling trends hold. Add this possibility to an already expensive market and you can throw all alphabet predictions you’re reading out the window.

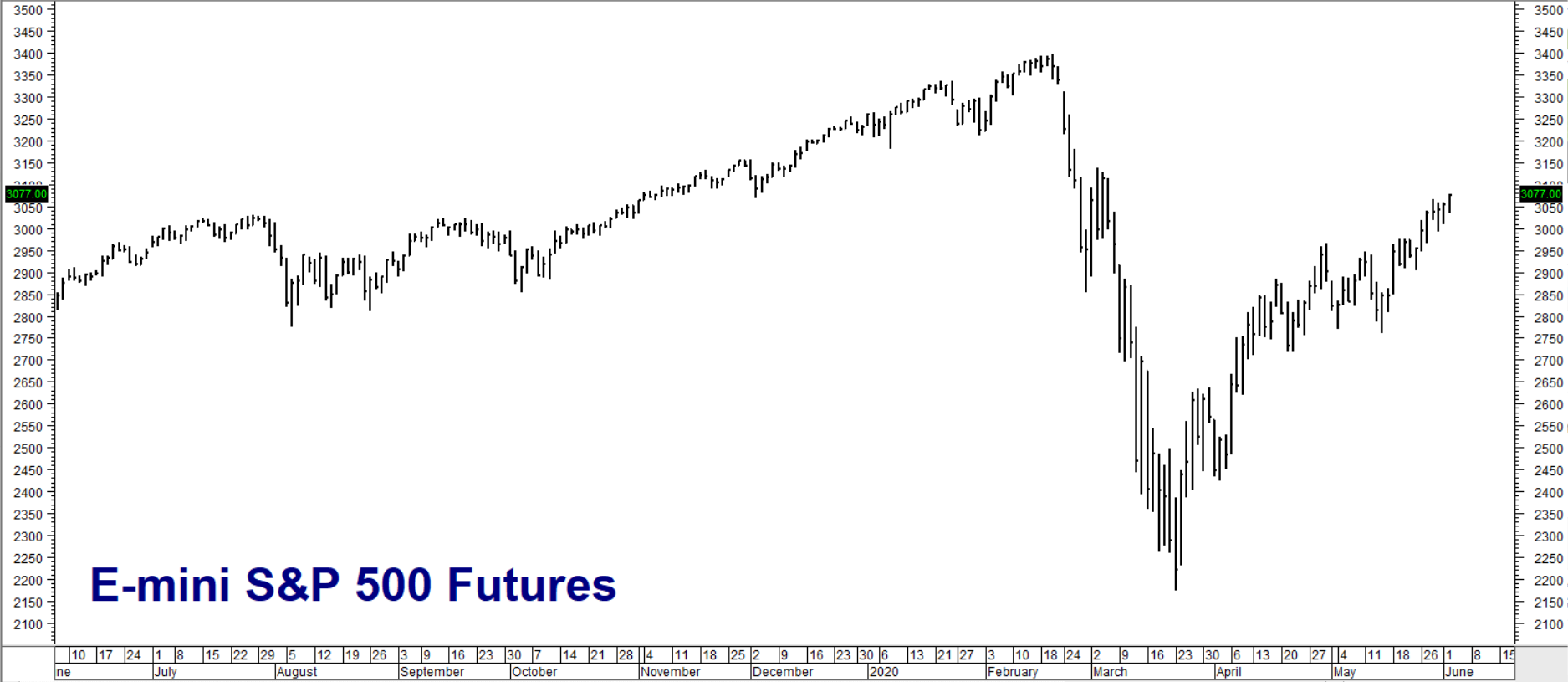

Data Source: Reuters/Datstream

This is why we believe the current rally in stocks, while certainly impressive, will ultimately prove ephemeral. RMB Group trading customers should consider hedging some or all of their stock market exposure by establishing fixed risk, bear put spread strategies using the E-mini S&P 500 put options traded on the CME. Speculators can use the same type of strategy to capitalize on the eventual resumption of the COVID-19 decline. Our ultimate target is a retest of the March lows just below 2200.00 in the nearby futures contract. Contact your RMB Group broker for up-to-date recommendations and prices.

Please be advised that you need a futures account to trade the markets in this post. The RMB Group has been helping our clientele trade futures and options since 1991. RMB Group brokers are familiar with the option strategies described in this report. Call us toll-free at 800-345-7026 or 312-373-4970 (direct) for more information and/or to open a trading account. Or visit our website at www.rmbgroup.com. Want to know more about trading futures and options? Download our FREE Report, the RMB Group “Short Course in Futures and Options.”

* * * * * * * *

The RMB Group

222 South Riverside Plaza, Suite 1200, Chicago, IL 60606

This material has been prepared by a sales or trading employee or agent of R.J. O’Brien & Associates (“RJO”)/RMB Group and is, or is in the nature of, a solicitation. This material is not a research report prepared by a Research Department. By accepting this communication, you agree that you are an experienced user of the futures markets, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions.

DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION.

The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from trades and statistical services and other sources that RJO/RMB believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades.