Unfortunately for the bulls, gold has been anything but good. The Midas Metal has spent the last 6 years putting traders and investors to sleep. It has oscillated between a high of $1,434 per ounce in 2013 and a low of $1,045 per ounce in late 2015. While there have been periods of excitement for both bulls and bears, they were short-lived. Nearly every meaningful move has ended in an abrupt reversal. But things appear to be changing…

Fears of a global slowdown – due to Europe’s failure to generate growth despite years of negative interest rates and President Trump’s seemingly endless tariff wars – have driven US interest rates down to levels inconceivable just 8 months ago. Yesterday’s 2.076% yield on US 10-year Treasury notes represents a collapse of 36% from the 3.213% they yielded on November 6, 2018. JP Morgan is calling for yields to fall even further, predicting a decline to 1.75% – just above historical lows.

What does this have to do with the price of gold? Lower interest rates reduce the opportunity cost of owning physical gold. Since gold earns no interest, the amount of interest a dollar invested in gold would make if invested in safe interest-bearing investments becomes part of the carrying cost of owning gold. It’s a lot easier to justify buying gold when you are giving up less. Reduced carrying costs tend to make gold more attractive.

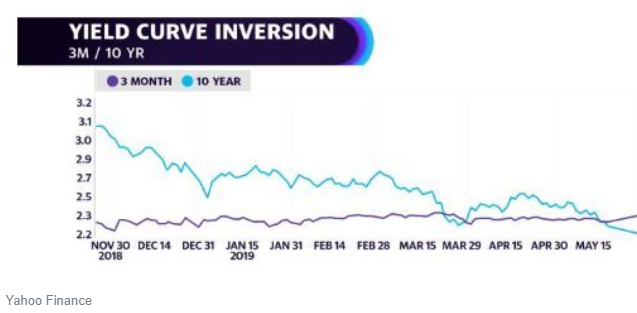

Another source of fear is the relationship between the Ten-year T-note yield and the 3 month T-Bill yield known as the “yield curve.” When Ten-year yields sink below 3 month yields, the yield curve becomes “inverted.” (See chart above.) Yesterday’s 2.076% Ten-year Treasury yield was 25 basis points (1/4 of 1 percent) lower than Friday’s 2.33% 3-month T-Bill yield. This makes the curve the most inverted it has been in a long time.

Investors normally want a better return for tying up their money for longer periods. One of the few reasons why investors would be willing to accept less money for longer term debt is the expectation that yields will drop even further in the future. What could cause this to happen? A recession or another global calamity.

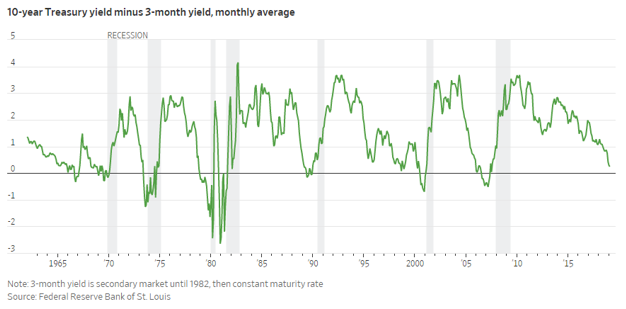

The bond market is nearly always better than the stock market at sniffing out danger. The inverted yield curve is not a perfect leading indicator, but as the long-term chart above illustrates, it is pretty darn reliable as far as indictors go. While not every yield inversion leads to recession, every modern recession was either signaled by or accompanied by one. Right now, the yield curve inversion is telling us to expect big trouble down the road for both the stock market, and the economy.

Gold Reprises Its Traditional Role as a Fear Gauge

Gold has been effective calamity insurance for over 2,000 years. Gold tends to do best when investors believe the financial status quo is coming apart. Consequently, we are not surprised to see that the incredible rally of the past three days has coincided with the flight-to-safety message being broadcast by the inverting yield curve. Both signals are flashing “fear” in big yellow letters.

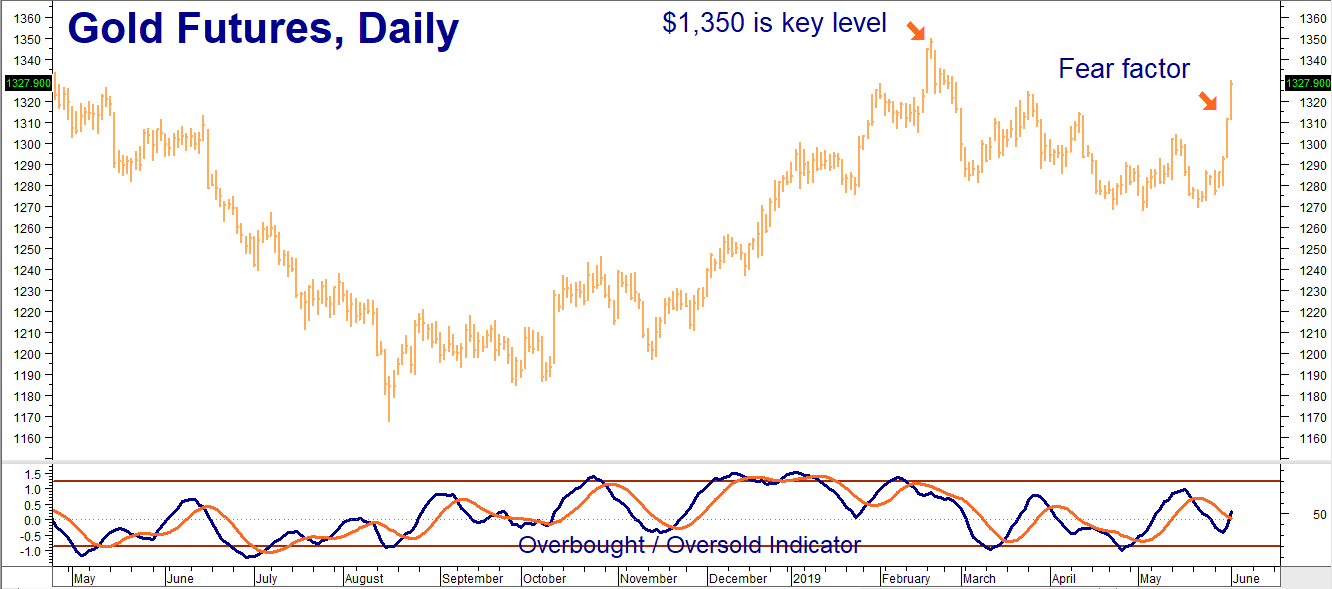

Gold’s last swing high at $1,350 per ounce (see chart below) represents the next level of resistance. Gold could be “off to the races” should the bulls take this level out in any significant way.

Data Source: Reuters

Interest rates are not the only source of fear in today’s markets. What investors fear most is uncertainty. Investors are starting to worry that Trump’s “trade by tweet” policies will result in a long, drawn-out trade war that could push the global economy into recession. It is akin to what the Smoot Hawley Tariff Act did just prior to the Great Depression.

Both the stock market and investors have not been too worried about trade until recently. They figured the Administration’s bravado was merely a negotiating tactic and that agreements, particularly with China, would be forthcoming prior to next year’s election cycle. The longer the trade war lingers, the more economic damage and investor uncertainty it could produce.

A long trade war also has the potential to upend the economic and political order which has underpinned the global economy since the fall of the Soviet Union. Major cracks have already occurred. Economic populism and nationalism have taken hold in Europe and the United States, threatening the smooth functioning of the global economy. While there are certainly many cheering on the demise of the status quo, its undoing will not be without severe and potentially catastrophic consequences.

Our biggest concern is overall investor complacency. The stock market sells off on bad trade news, recovers on the mere rumor of an agreement, and then repeats this same behavior over and over. Stock investors are acting like the townsfolk in the fairy tale, “The Boy Who Cried Wolf.” They hear so many false alarms that they become utterly defenseless when the wolf finally arrives.

Is gold following the bond market’s lead? It sure looks like it. Central banks have been loading up on gold, purchasing 145.5 tons so far this year – 68% more than the same time last year. Time will tell whether or not this is a good strategy. One thing is certain: gold looks a heck of a lot better chart-wise than it did a few days ago.

Gold Looks Way Better Than Three Days Ago

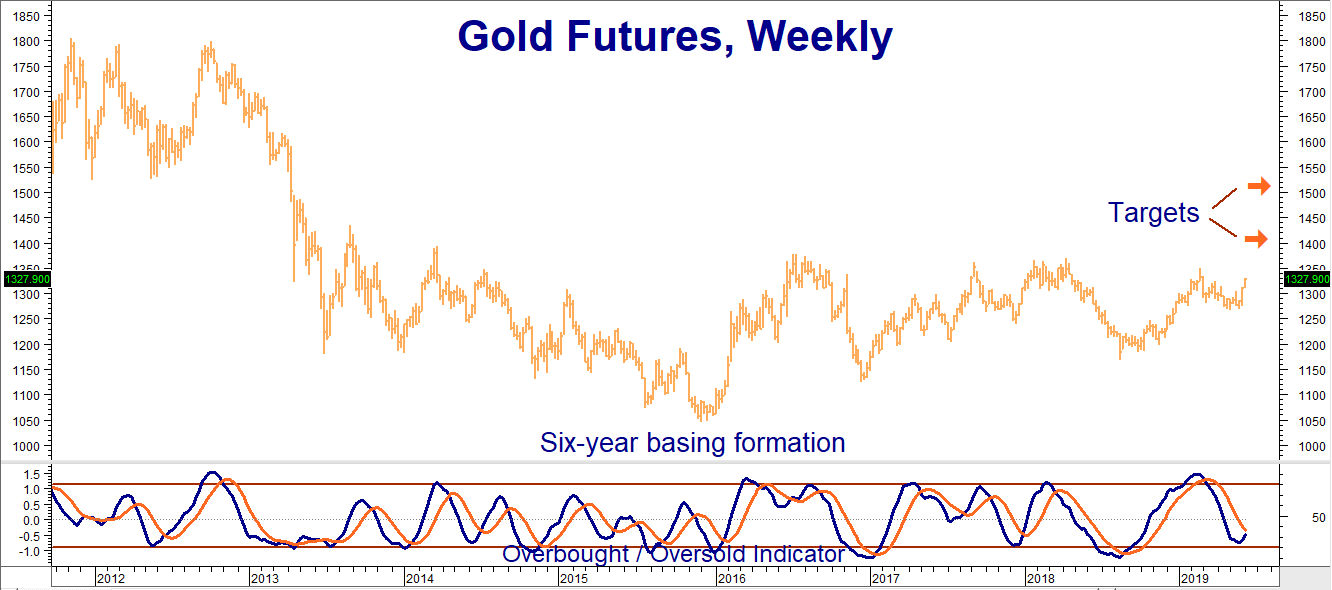

Gold has formed a six-year base and is rallying from severely oversold levels on both a daily and weekly basis. As we mentioned earlier, the swing high of $1,350 per ounce is a key level short term. A few closes over $1,350 would set the stage for an assault of the August 2013 high of $1,434 per ounce. Take this out, and our second $1,500 per ounce target comes into play.

Data Source: Reuters

RMB Group trading customers who took our suggestion in October 2018 to buy December 2019 $1,400 / $1,450 bull spreads in the COMEX gold option for $600 or less should continue to hold, looking for a possible test of resistance at $1,434 per ounce prior to option expiration on November 25, 2019. These spreads closed for $720 yesterday.

Consider adding June 2020 $1,450 / $1,500 spreads to cover a potential move to our $1,500 objective by June option expiration on May 26, 2020. The June 2020 spreads closed yesterday for $750. Pay no more than this. Your maximum risk on both is the amount spent plus transaction costs. Each trade has the potential to be worth as much as $5,000.

Those without a position in gold may want to consider combining both. Check with your personal broker for recent pricing, as well as other bullish strategy suggestions suited to your risk and market outlook.

Please be advised that you need a futures account to trade the markets in this post. The RMB Group has been helping its clientele trade futures and options since 1991 and are very familiar with all kinds of option strategies. Call us toll-free at 800-345-7026 or 312-373-4970 (direct) for more information and/or to open a trading account. Or visit our website at www.rmbgroup.com.