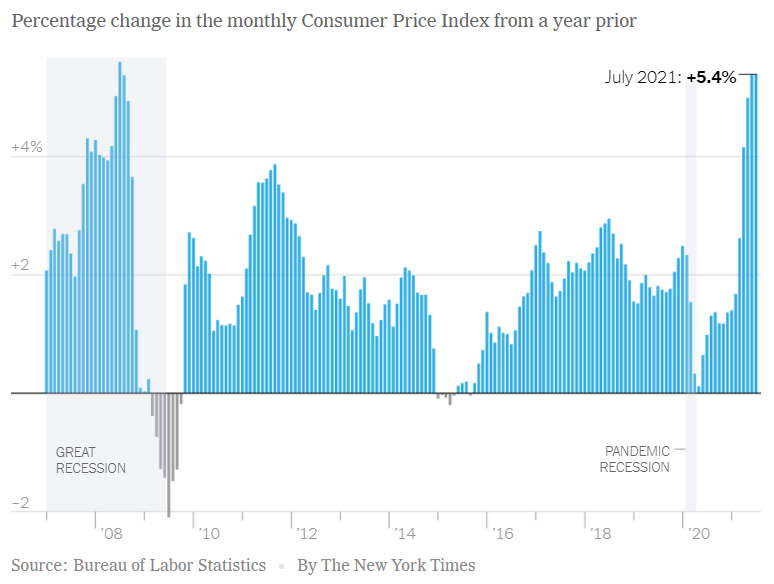

Strong demand continues to drive the price of essential goods higher. The average price of a home is up 18.6%. The price of gas is skyrocketing. So are the costs for basic staples like grain, sugar and coffee. Inflation signals like the Consumer Price Index (CPI) have been flashing bright red for months, yet bonds refuse to give up the ghost. Why?

A large part of the answer has to do with the same Fiscal stimulus partially responsible for today’s inflationary environment. Government Covid relief plans funneled roughly $1.6 trillion into the bank accounts of individual and businesses in just the past year hoping to counter the deflationary effects of the pandemic. This is $900 billion more than the entire $700 billion TARP stimulus used to bailout banks after the 2008 housing collapse.

Roughly $830 billion of Covid relief cash went directly into the bank accounts of individuals. Another $800 billion poured into businesses. Yet another $570 billion (not counted as “relief funds) was spent on expanded unemployment benefits. This incredible influx of money fattened demand deposits held in banks, which jumped 30% compared with the period before Covid.

Banks Are Buying Treasuries

Banks are lending institutions. They profit from the difference between the interest they receive for loans and the rate they pay for deposits. Banks lend out dollars sitting in deposit accounts and use the interest received to pay for servicing these accounts, cover other fixed costs and generate a profit. Failure to lend at an interest rate high enough to cover all three will cause problems. Banks are paying virtually zero for deposits now – but the lack of demand for higher interest loans is proving to be a problem anyway.

Consumers, flush with stimulus cash, are not borrowing enough to cover the carrying costs of the cash they have on deposit in banks. They are doing the opposite – using their stimulus money to pay down debt. The shortage of key components like computer chips that run critical systems in automobiles (and other products) is choking demand for business loans used to finance inventory. Lack of product means a lot less inventory needing to be financed.

Reduced loan demand forces banks to buy Treasuries in order to generate income from the incredible influx of cash sitting in their deposit accounts. US Treasuries are guaranteed by the good faith of the Federal Government. Earning 1.3% on a 10-year Treasury note is better than no yield at all.

Banks bought approximately $150 billion worth of Treasuries in the first quarter. Divide that by the three months that make up a quarter and you get $50 billion. Add this to the $80 billion of Treasuries the Fed is buying every month, and the failure of the bond market to sell off in response to high inflation starts to make more sense. Bond prices move inversely to yield. Fed and bank demand is driving up prices and driving down yields.

Covid, Covid, Covid

Why hasn’t the Fed “tapered” its purchases to offset some of the stimulus-inspired demand from banks? We suspect there are two reasons. The first has to do with Covid. The second also has to do with Covid – albeit indirectly.

The Delta variant’s rapid spread is throwing a wet blanket on expectations of a fast economic recovery. It also adds credence to Fed Chairman Powell’s argument that inflation will be “transitory” and revert back to the Fed’s 2% target once pre-pandemic employment levels are achieved and global supply of key commodities and components catch up with demand.

The problem is none of this is actually happening. Unemployment remains above pre-Covid levels despite 9 million jobs being unfilled. Chip shortages continue to plague many industries and are expected to be long-term. Worse still, the incredible increase in productivity which accompanied the last 30-years of globalization, and helped hold inflation at bay, is being disrupted by both Covid and economic balkanization due to rising nationalism. “Just-in-time” doesn’t work well anymore. For some industries, it doesn’t work at all.

“Transitory” Inflation Not Going Away Anytime Soon

Covid-caused inefficiencies in the global economy will continue even after the pandemic is finally controlled. It will take a fair amount of time to fine-tune supply chains and right skewed labor markets. But Covid must be controlled first. This is taking far longer than everyone expected. It leaves plenty of room for inflation to gain a foothold.

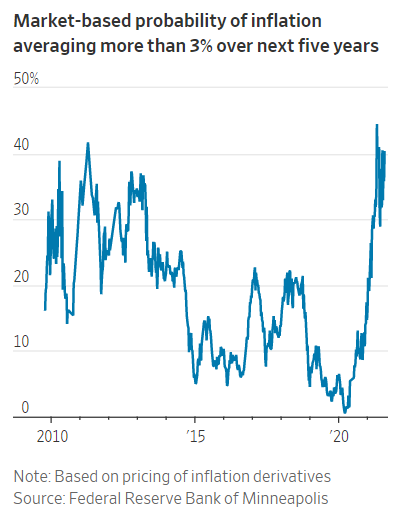

The probability of this happening is soaring, reaching levels not seen since the aftermath of the stimulus after the 2008 housing collapse. The amount of Covid stimulus already injected is over three times the amount spent in 2008 and 2009. We expect more to come.

Ten-year Treasuries currently yield 1.3%. An inflation rate of 3% makes their real yield minus 1.7%. This makes Treasury debt purchased a guaranteed loser in any future in which inflation exceeds 1.3% — including the Fed’s preferred inflation target of 2%. T-bond and T-notes yields may not reflect this now, but the end of direct deposit stimulus and Fed tapering could mean big changes soon.

Coming Soon: End of Direct Stimulus & Start of Fed Tapering

The era of direct stimulus is over. Democrats, eager to get both infrastructure bills passed, cannot afford to push any more direct relief. Doing so would be politically devastating and threaten the passage of both.

Money slated for infrastructure will make its way into the economy over the course of a decade and will not be injected into banks directly, reducing the need for banks to put it to work earning a return. We expect cash held in deposit accounts to shrink as Federal direct deposit relief money dries up, removing pressure on banks and causing their purchases of Treasury debt to drop.

Progress on Covid will also play a role. Companies and corporations are rushing to establish vaccine mandates now that Pfizer’s jab has formal FDA approval. We believe this will significantly increase the number of people vaccinated and bring the US closer to getting the pandemic under control.

Lower infection and hospitalization rates will re-open the door closed by the Delta variant and make “tapering” part of the bond conversation again. Five of the Fed’s Regional Bank Presidents have already indicated their desire to cut back on Treasury bond and note purchases. Some have indicated an interest in ending these purchases by the close of 2022 instead of 2023.

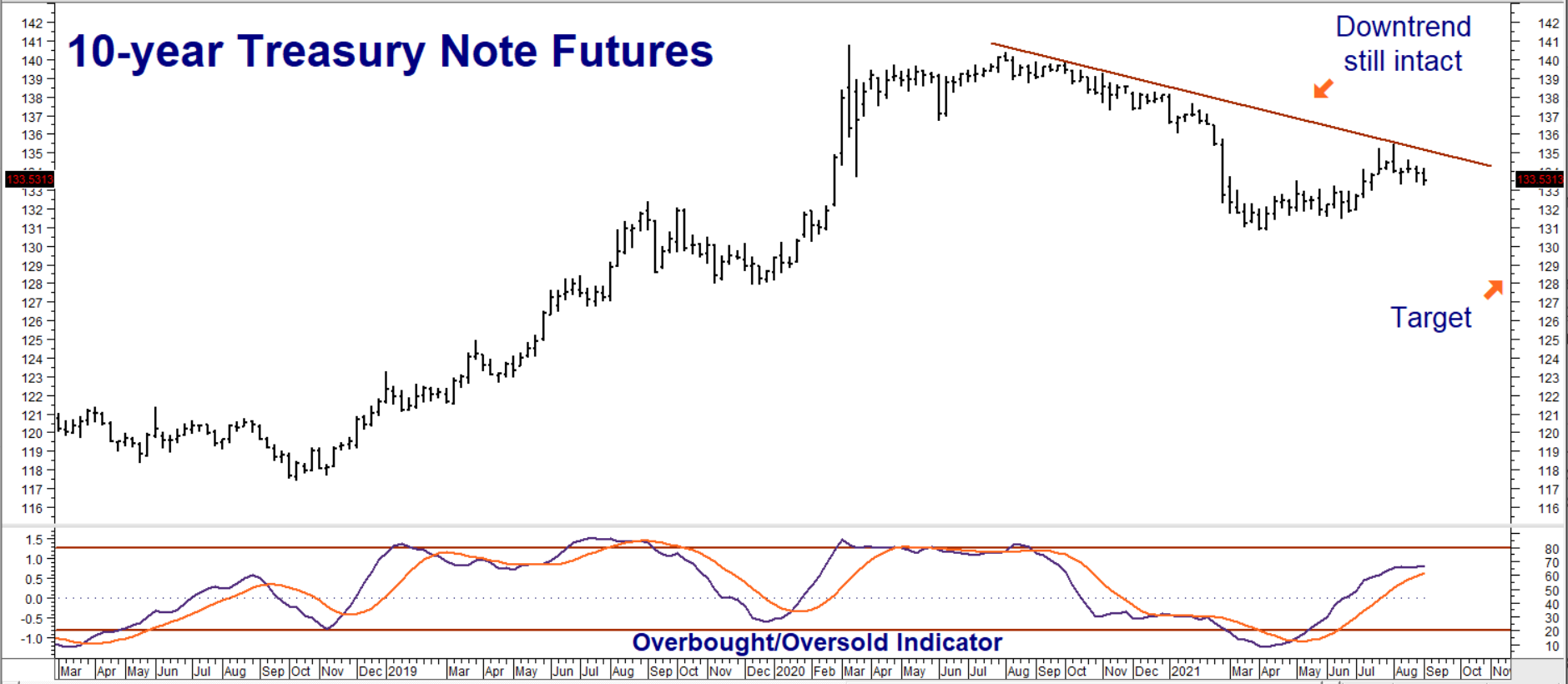

Consider a Low-Cost Bear Position in T-Notes

Combine persistent inflation, the end of direct stimulus and the likely tapering of Fed bond purchases, and you get a powerful formula for lower prices. Add in today’s overbought conditions (as well as the inability of bulls to negate the current downtrend, despite big Fed and bank buying), and you wind up with a nice set-up for a bearish trade.

Data Source: Reuters/Datastream

Reasonably-priced put options give us the opportunity to take a stab at a low-cost bearish position in T-notes. RMB Group trading customers may want to consider purchasing the December 132-00 put options traded on the CME. Look for future prices to fall to our downside target of 128-00 prior to option expiration on November 26, 2021.

December 2021 132-00 puts settled for $515.63 each on Thursday, September 2nd. Your maximum risk is the price paid for your put(s) plus transaction costs. These puts will be worth at least $4,000 should December T-note futures hit our 128-00 target prior to November option expiration. Prices can and will change so contact your RMB Group trading professional for the latest.

Please be advised that you need a futures account to trade the markets in this post. The RMB Group has been helping our clientele trade futures and options since 1991. RMB Group brokers are familiar with the option strategies described in this report. Call us toll-free at 800-345-7026 or 312-373-4970 (direct) for more information and/or to open a trading account. Or visit our website at www.rmbgroup.com. Want to know more about trading futures and options? Download our FREE Report, the RMB Group “Short Course in Futures and Options.”

* * * * * * * *

The RMB Group

222 South Riverside Plaza, Suite 1200, Chicago, IL 60606

This material has been prepared by a sales or trading employee or agent of R.J. O’Brien & Associates (“RJO”)/RMB Group and is, or is in the nature of, a solicitation. This material is not a research report prepared by a Research Department. By accepting this communication, you agree that you are an experienced user of the futures markets, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions.

DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION.

The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from trades and statistical services and other sources that RJO/RMB believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades.