In our latest blog series “Investing in the Age of Trump”: Parts One, Two and Three, we examined the Trump phenomenon, assessed his odds of winning and determined that he would be the Republican nominee for U.S. president. What we didn’t foresee was how easy it would be and how quickly the never-Trump Republican establishment would roll over and expose their soft underbellies to the tough-talking New Yorker. They proved what the blue collar, Republican base has been saying all along: their traditional leadership is all bark and no bite.

A coalescing Republican Party combined with the bitter battle between Bernie and Hillary supporters substantially increase the odds of a Trump victory in November. In Part One of our blog series we identified Donald Trump as a “black swan”. This is an unanticipated event which can have dramatic and unexpected consequences. Virtually no one thought Trump had a chance three months ago. Now he is the de-facto Republican nominee with a real possibility of winning it all.

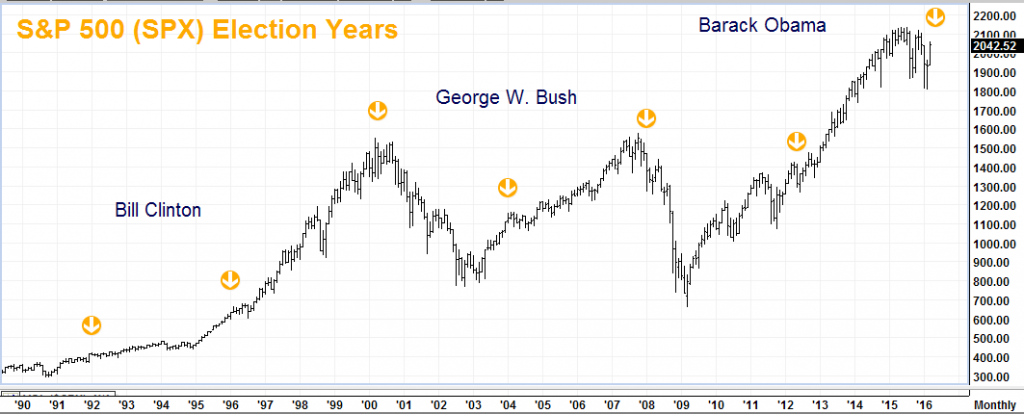

We started Part Three of our Trump series with the chart above. It shows the stock market reaction to the last six election cycles, noting that “The similarity of the current price action to the end of both the Clinton and Bush terms is sobering to say the least. Election year consequences are relatively benign when the incumbent party retains power, but downright nasty when it doesn’t.” Even if the Republican nominee wasn’t Donald Trump, a switch in presidential power from one party to another, particularly after an 8-year term, is not the best of all possible scenarios for stocks.

Since the nominee likely will be Mr. Trump, the word “nasty” does not even begin to describe the potential carnage if the stock market starts believing he could win in November. Yesterday’s bearish price action could be a sign that this is happening already.

Trump Victory Likely to Send Stocks Swooning

The problem is a Hillary Clinton victory is already priced into the stock market. Secretary Clinton is a known quantity. Markets tend to respond much better to what they know – as flawed as it may be. Stock markets hate uncertainty. As we stated in Part Three, “Secretary Clinton is part of the political establishment. She is stable, relatively predictable and expected to win…

“Combine a “Black Swan” Trump victory with the recent tendency of the S&P 500 to decline dramatically following a transfer of power and stocks could swoon big between now and election day – especially if Clinton’s victory narrative is threatened in any significant way.”

Mr. Trump’s penchant for changing his mind and his positions on any given topic, at any given time, are the very definition of uncertainty. The most dangerous of his economic ideas – at least as far as the stock market is concerned – is his plan to place tariffs on Chinese and Mexican imports. Restricting trade is nearly always bad for the global economy and for stocks. The Great Depression that began with the 1929 crash was made much worse by the Smoot Hawley Tariff Act of 1930.

Trump is Not the Only Threat to Stocks

- At 85 months, the current bull market is the third longest in history. If it is still intact on July 10, it will be second longest. The longest bull market on record was 113 months and occurred during Bill Clinton’s two terms in office. While this doesn’t mean stocks can’t go higher, it confirms that the current bull market is “long in the tooth.”

- The stock market is expensive based on numerous metrics. The current price / earnings (PE) ratio for the S&P 500 is 23.71. Compare this to a median PE of 14.62 and a mean of 15.59. The cyclically-adjusted PE ratio (CAPE) favored by many analysts because it smooths market data is currently 26.11, compared with its long term average of 16.61.

- Earnings are suffering – especially in retail and formerly high-flying sectors like tech and bio-tech. Market bellwether Apple has been hit particularly hard, falling 16.6% in just the last month.

Add the real potential of a Trump victory to an already sketchy market and you increase the potential for a big disruption in the next six months. Stock market performance is all about perception. The less confidence the market has in a Clinton victory, the weaker it will get. The speed at which the Republican Party is falling in line behind Trump reduces the odds of a Hillary Clinton victory. Her narrative is being threatened and stock prices are reacting accordingly.

We Still Like Managed Futures…

In Part Three of our Trump series we suggested looking into individually managed futures accounts run by Commodity Trading Advisors (CTAs) because they have a solid history of providing investors with performance-smoothing diversification – especially during times of crisis. We favor this approach because of the potential for commodity CTAs to perform well in both up and down stock markets. We will examine the performance of one of the CTA combinations we are tracking and compare it to the performance of the S&P 500 in a future blog post.

Give RMB Group a call at 800-345-7026 or 312-373-4970 if you would like to learn more about the CTAs we are following right now. To find out how individually managed futures accounts can work for you, download our free booklet and accompanying video – Opportunities Outside the Stock Market.

… But Here’s Something You Can Do Right Now

If our analysis is right, stocks could begin a major downward correction at any point during between now and November. If you are looking for a way to get short the market and/or hedge your current stock holdings for a fairly small capital outlay, we have a potential solution.

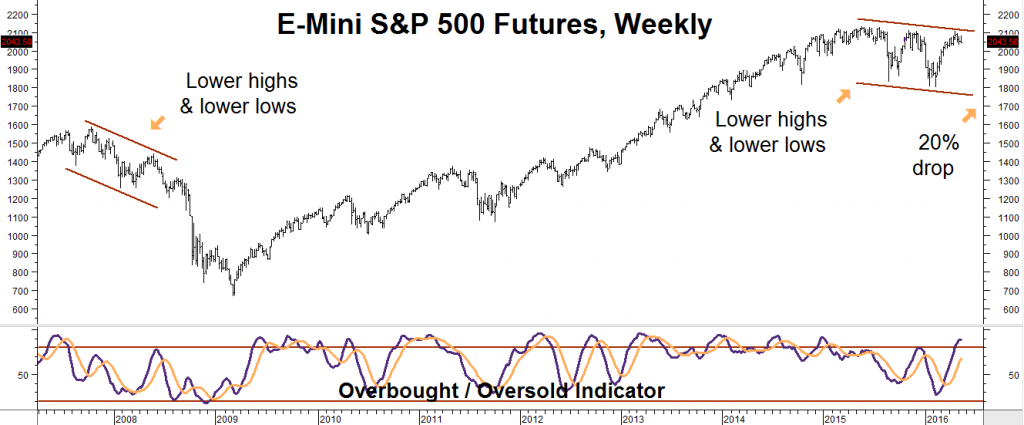

On the chart below, note the similarity of the price action just prior to the 2008 election with current price action. A series of lower highs and lower lows was signaling a potential market top well before the wheels came off after the Lehman collapse. Could a similar thing be happening now? Combine today’s political reality with an expensive, long-in-the-tooth bull market with faltering earnings, and you get a formula for potential disaster.

We hope we are wrong, but we see the potential for a 20% drop from the S&P 500’s closing high prior to the November election. As you can see on the chart, 20% is just a little lower than the bottom of the current trading range and definitely achievable given the current market environment.

Multi-billionaire investor George Soros shares this outlook. He just doubled his bearish bet, purchasing put options covering 2.1 million share of SPY. We are going to use put options as well – but instead of using the SPY we are going to construct our bearish strategy using the super-liquid E-mini S&P 500 options market.

RMB trading customers should consider buying December E-mini S&P 500 bear put spreads. We suggest buying the 1900 puts while simultaneously selling the 1700 puts for a total cost of $1,500 or less. Maximum risk on this position is $1,500 (plus transaction cost) per spread.

These “bear put spreads” could be worth as much as $10,000 should the S&P 500 close at or below 1700 (a drop of 20% from closing highs) on or prior to option expiration on December 16, 2016. They settled yesterday for $1,900 apiece, so we will need about a 1% bounce in the underlying index to get filled at our price.

Each spread covers roughly $103,000 in stock market value – so investors interested in hedging their portfolio should consider using this for reference. Please be advised that prices can and will change, so check with your personal RMB broker for the latest. He or she can tailor similar strategies to fit the risk profile that works best for you.

Getting Started

You need a futures account to trade the recommendations in this report. The RMB Group has been helping customers trade futures and options since 1984 and are very familiar with the strategies suggested in this report. Call us toll-free at 800-345-7026 or 312-373-4970 direct to learn more. We’ll send you everything you need to get started. You can also visit www.rmbgroup.com to open an account online.

If you are new to futures and options and want to learn more, download the RMB Short Course in Futures and Options. This easy-to-read guide covers all the basics. Call us toll-free at 800-345-7026 or 312-373-4970 direct for your free copy or go to our website at www.rmbgroup.com. Click the “Education Tools” tab at the top of the home page and scroll down to find the report.

—

The RMB Group

222 South Riverside Plaza, Suite 1200, Chicago, IL 60606

This material has been prepared by a sales or trading employee or agent of R.J. O’Brien and is, or is in the nature of, a solicitation. This material is not a research report prepared by R.J. O’Brien’s Research Department. By accepting this communication, you agree that you are an experienced user of the futures markets, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions.

DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION.

The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from trades and statistical services and other sources that R.J. O’Brien believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades.

This report was written by Investors Publishing Services, Inc. (IPS). © Copyright 2016 Investors Publishing Services, Inc. All rights reserved. The opinions contained herein do not necessarily reflect the views of any individual or other organization. Material was gathered from sources believed to be reliable; however no guarantee to its accuracy is made. The editors of this report, separate and apart from their work with IPS, are registered commodity account executives with R.J. O’Brien. R.J. O’Brien neither endorses nor assumes any responsibility for the trading advice contained therein. Privacy policy is available on request.