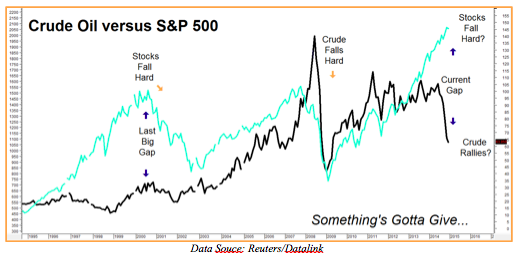

The relationship between crude oil and the US stock market is one of the most important on the board because both are a reflection of the global economy. American stocks are a leading indicator – rising on the expectations of good times ahead and falling when the market smells trouble. A booming economy increases oil and energy demand leading to higher crude prices. Recessions reduce energy demand causing prices to fall. This is why crude oil and stocks track together most of the time.

The chart below shows the relationship between oil futures and the S&P 500 stock index since the mid 1990s. These markets rarely move in opposite directions and when they do, it doesn’t last long. Stocks fell hard to meet crude prices after going their separate ways in 2001 and 2002. Crude fell hard to meet stock prices in 2008 and 2009. The gap between the two has never been wider than right now. This is a big anomaly and should be paid attention to.

We believe crude may be leading again – only this time to the downside. The reason? The shale oil industry has been one of the biggest sources of American economic growth. Low crude oil prices damage the profitability of the shale industry with negative ramifications that have the potential to extend into the economy as a whole.

A big portion of shale oil exploration was funded by high yield debt which is currently trading for a fraction of par value because of the huge decline in crude. Should this debt stay on the path to default, it could send shocks waves into the broader market, damaging this long-in-the-tooth bull and undermining confidence. Shale debt is illiquid and hard to trade just like the pre-packaged, subprime mortgage debt blamed for the 2008 Lehman collapse.

Stocks are Expensive & Oil is Cheap

If one assumes that the historical correlation between oil and stock prices isn’t irrevocably broken, then something’s got to give. Stocks are either too expensive, crude oil is too cheap or both. One thing that sticks out is the power of gravity. The relationship between the stock market and crude oil has gotten seriously out of whack only twice in the past 20 years. In both cases the overpriced market fell to meet the underpriced one. In 2001 it was the stock market falling to meet crude. In 2008 oil fell precariously to meet a stock market decimated by the housing crisis.

Will stocks fall to meet crude oil again? We don’t know. What we do know is stocks are getting uber-expensive at the same time crude is getting super cheap. We believe this discrepancy has reached the point of becoming a tradable event – especially if you have a speculative bent. While we are not recommending dumping your stocks here, it is important to remember that gravity is a powerful force once it takes hold.

We don’t know when crude oil / stock market relationship will revert to the mean but if history is any guide, it will. There are three ways this can happen:

- Stocks will decline sharply in line with the cost of crude once the market realizes the deflationary and destabilizing effect of low crude oil prices. New oil and gas well permits dropped 40% in November. Expect more negative surprises down the road. Shale companies issued a boatload of high-yield debt to finance drilling operations. Much of this will end up in default should oil prices remain at today’s depressed levels. Holders of that debt will start puking it out at steep haircuts into an already illiquid market causing huge disruptions and damaging market confidence. Remember the last time holders of toxic, illiquid, mortgage debt tried to do the same thing? It wasn’t pretty. It won’t be this time either.

- Crude oil will rally either all at once due to some unforeseen geopolitical occurrence or more slowly in response to reduced output by high cost producers.

- A combination of scenarios 1 and 2: War with Russia, a pre-emptive strike on Iran (should current talks fail) or numerous other scenarios could send oil prices skyrocketing and stocks tumbling simultaneously.

Not only has the geopolitical risk premium disappeared entirely from the crude oil market, it has essentially gone negative. It could reappear virtually overnight –tacking $5 to $10 per barrel to the cost of oil in the process.

How to Play It

The old saying, “markets can remain irrational longer than you can remain solvent” certainly applies here. That’s why we are recommending RMB Group trading customers consider combining a bearish, limited risk option strategy in stocks with a bullish, limited risk option strategy in crude, looking to capitalize on a regression to the mean in both.

If you were to force us to choose one over the other we would favor the bearish stock index position over the bullish crude oil position but realize either one (or both!) could work given the right circumstances.

Right now we are looking at a bearish position using March E-mini S&P 500 put options, risking around $700 plus transaction costs for a potential payoff of $5,000 should stocks drop 10% or more from current levels by mid-March.

We can combine this with a bullish strategy in crude oil using April NYMEX call options with a cost and risk of right around $500 and a potential payoff of $5,000 should crude make it back to $80 per barrel prior to option expiration on March 17. This may sound like a big hill to climb until you remember that crude oil traded at $80 per barrel just 4 weeks ago.

Our maximum risk on both positions is roughly $1,200 (plus transaction costs) with a potential payoff of $10,000 should crude rally and stocks decline at the same time. However both do not need to happen for this trade to be successful. A big selloff in stocks or big corrective equivalent rally in crude would be enough to cover the $1,200 cost of the position and then some. This kind of flexibility and risk control is why we love options.

E-Mini S&P 500 and crude oil futures are volatile and can turn on a dime so check with your personal RMB Group broker for our latest on this strategy and to get up-to-the-minute pricing.

If you don’t have an RMB Group trading account and would like to know more about this or any other “Big Move” strategy, call 800-345-7026 toll free or 312-373-4970 direct. You can also email suerutsen@rmbgroup.com or visit us online at www.rmbgroup.com.