It’s official: the UK is leaving the EU. And while the agreement gives both parties a year to work things out, the way business is done in Europe will change substantially. Most of the speculation about the effects of Brexit has involved the UK and the British Pound (or Sterling.) This has caused it to fluctuate in the run-up to Brexit’s inevitable outcome. Meanwhile, nobody seems to be watching the euro.

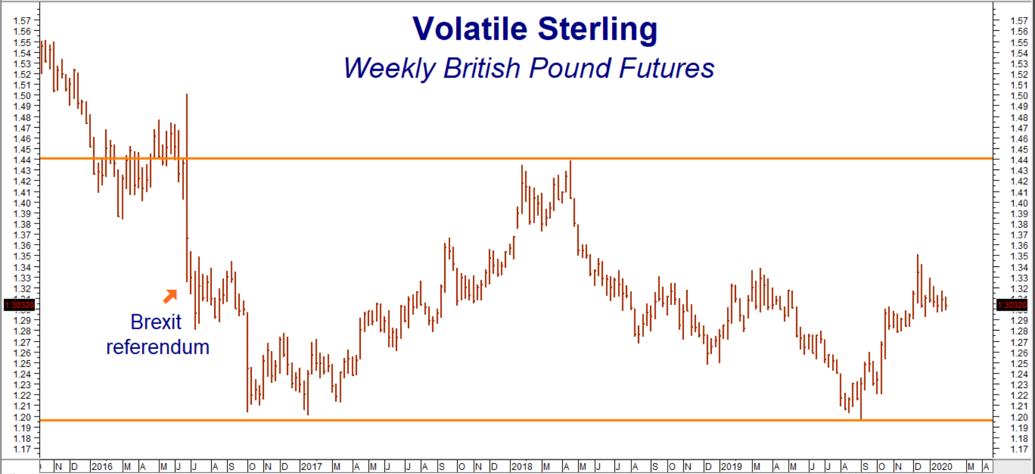

This fluctuation is evident in the chart of British Pound futures below. Sterling has bounced back and forth in a wide trading range since the June 23, 2016 Brexit referendum. It has climbed as high as $1.5090 just before the vote, and sunk as low as $1.1965 two years later. Some of this volatility is built into the British Pound options traded on the CME, but not as much as we’d expect.

Data Source: Reuters/Datastream

“Straddles” Measure Market Volatility

How do we know this? We look at the price of at-the-money “straddles”. Straddles involve the purchase (or sale) of an equal number of put and call options with an identical strike price closest to the price of the underlying stock or commodity. Buyers of options pay money for the right, but not the obligation, to be long at the strike price of a call, or to be short in the case of a put. The key phrase is “but not the obligation.” All an option buyer has at risk is the cost of the option plus whatever transaction costs he or she incurs.

Sellers of options receive money in exchange for the obligation to be long or short. Call sellers have an obligation to be short at the strike price of calls they sell and to be long at the strike of puts they sell. Options sellers are making a bet that they will not have to perform their obligations and will get to keep the money received from option buyers. This allows us to determine how much volatility option traders expect over a given timeframe by adding the prices of at-the-money calls and puts together.

Here’s an example: June 2020 British Pound futures settled at $1.3078 on Wednesday; June BP $1.3100 calls settled at $0.0183 and June $1.3100 puts settled at $0.0205. The sellers of this “straddle” were willing to receive $0.0388 for the obligation to be both long and short the British Pound at $1.3100, which means they expect Sterling to move no more than the $0.0388 they we willing to sell the straddle for. The sellers of this straddle expect the pound to stay in a range between $1.3488 on the upside and $1.2712 on the downside.

Divide the $0.0388 combined price of the put and call options by the $1.3100 strike price of both and you get .0296. This means as of settlement on January 29, 2020, option traders expected the British Pound to move no more than 2.96% by expiration of June options on June 5, 2020 – 126 days from now. With Brexit right around the corner, this seems low – especially given Sterling’s post-referendum history.

Euro Volatility is Extremely Low

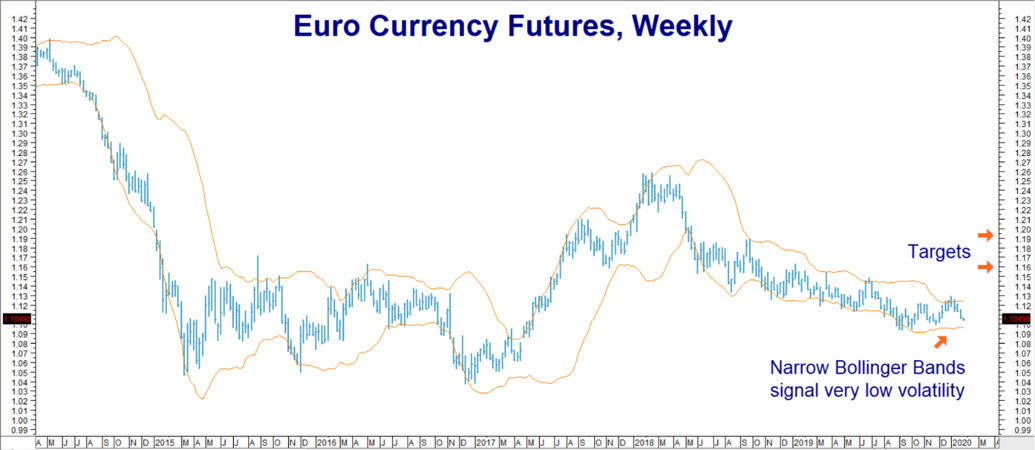

As tempting as a long position in British Pound calls may be, the euro looks even better for a number of reasons. The first is even lower volatility expectations. Using the same methodology outlined above, option traders expect the euro to move no more than 1.86% in the next 126 days. We don’t remember euro volatility ever being this low.

Data Source: Reuters/Datastream

Bollinger Bands measure a trading range two standard deviations above and below any given market. The narrow Bollinger Bands illustrated on the chart above are based on past market behavior. Euro option traders are extrapolating this abnormally quiet behavior into the future, making euro options extremely cheap in the process. We believe this is an opportunity for RMB trading customers to take inexpensive, limited risk positions in euro call options.

The Bullish Case for the Euro

Our original plan was to take advantage of the euro’s ridiculously low volatility by recommending the purchase of both puts and calls (similar to what we recommended in our blog post on sugar last year). However, with the Fed likely “on hold” until after the presidential election – and the potential of that election to be extremely divisive and negative for the United States and the dollar – we decided on establishing a long position using euro call options instead. We like a little contrarian spice, so the fact that virtually no one expects Brexit to be good for the EU sealed the deal.

Our original plan was to take advantage of the euro’s ridiculously low volatility by recommending the purchase of both puts and calls (similar to what we recommended in our blog post on sugar last year). However, with the Fed likely “on hold” until after the presidential election – and the potential of that election to be extremely divisive and negative for the United States and the dollar – we decided on establishing a long position using euro call options instead. We like a little contrarian spice, so the fact that virtually no one expects Brexit to be good for the EU sealed the deal.

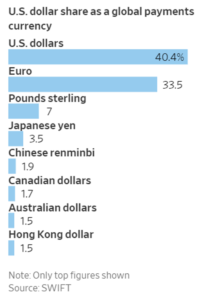

The US dollar will continue to remain the world’s preferred currency. However, there is only one other fiat currency that can pick up the slack should the US begin to lose its allure as a safe haven: the euro. At 57.5%, the euro is the biggest component of the US dollar index. It is also responsible for 33.5% of global payments, second only to the US dollar. No other currency comes close.

ECB Dove Takes Wing

Noted monetary policy dove Mario Draghi (architect of the EU’s negative interest rate policy) has flown the European Central Bank coop, replaced by pragmatist “owl” Christine Lagarde. Ms. Lagarde witnessed firsthand the relatively paltry effects of ECB monetary policy on European prosperity while chief of the IMF. Now as president of the European Central Bank, she has decided to call for fiscal stimulus by EU member nations instead. Whether that will be effective remains to be seen.

The new ECB president’s reluctance to continue Draghi’s policies most likely means an end to ever-lower interest rates in Europe. European interest rates are actually starting to stabilize – and even rise in certain locations. We believe this will be positive for the euro.

With the euro trading just above the bottom of its 5-month trading range – and volatility about as low as we’ve ever seen – now might be the perfect time for a low-cost, fixed risk play on the continental currency using CME euro options.

RMB trading customers may want to consider purchasing June 2020 $1.1300 call options looking for the June futures to hit our initial $1.1600 target prior to options expiration on June 5. June CME $1.13 calls settled yesterday for 51 points or $637.50 each. Your maximum risk is the amount paid for your call option plus transaction cost. These calls will be worth at least $3,750 should June euro futures hit our $1.1600 objective prior to option expiration.

Please be advised that you need a futures account to trade the markets in this post. The RMB Group has been helping its clientele trade futures and options since 1991. RMB Group brokers are familiar with the option strategies described in this report. Call us toll-free at 800-345-7026 or 312-373-4970 (direct) for more information and/or to open a trading account. Or visit our website at www.rmbgroup.com. Want to know more about trading futures and options? Download our FREE Report, the RMB Group “Short Course in Futures and Options.”

* * * * * * * *

The RMB Group

222 South Riverside Plaza, Suite 1200, Chicago, IL 60606

This material has been prepared by a sales or trading employee or agent of R.J. O’Brien & Associates (“RJO”)/RMB Group and is, or is in the nature of, a solicitation. This material is not a research report prepared by a Research Department. By accepting this communication, you agree that you are an experienced user of the futures markets, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions.

DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION.

The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from trades and statistical services and other sources that RJO/RMB believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades.