Silver has a split personality: it is both an industrial and a precious metal. We examined this dichotomy in early February when gold and silver were heading in different directions and issued a buy recommendation because we believed silver was undervalued vis a vis its richer cousin. Our target of $30 per ounce was hit in late May. We believe it is time to consider re-entering this market on the long side again.

Silver has been losing ground to gold since late May, declining 10.7% compared to gold’s drop of 5.9%. The longer-term picture is even more out-of-whack. Gold continues to make new highs while its poorer cousin remains far from its all-time high of $49.56 per ounce in 2011. Silver still has plenty of catching up to do.

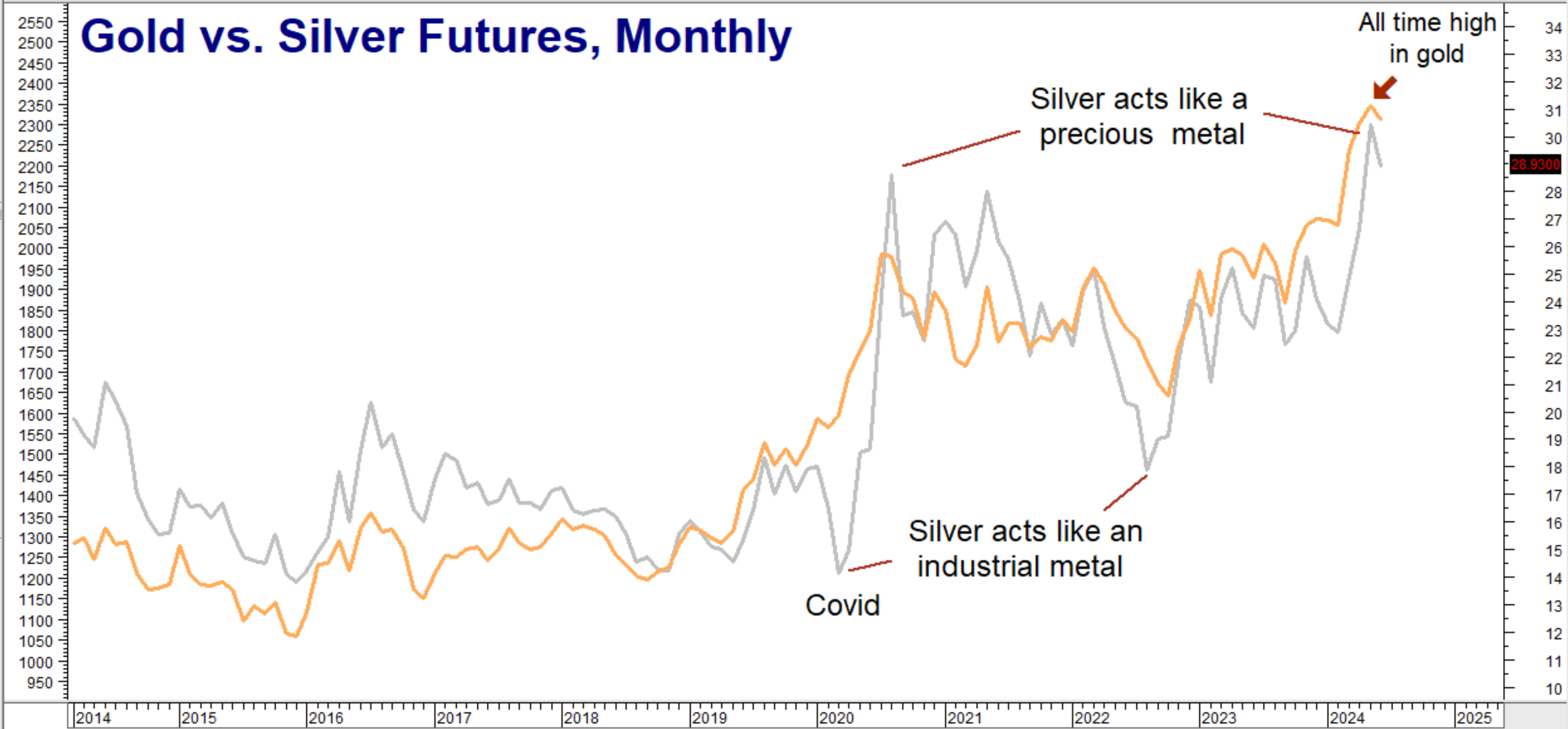

Data Source: Reuters/Datastream

Silver trades like an industrial metal most of the time, driven more by commercial supply and demand factors than investment interest. As the chart above illustrates, its reaction to Covid was a case in point. It acted like an industrial metal and declined sharply due to fears of an economic slowdown, then turned on a dime, and switched its identity to a precious metal in hot pursuit of gold.

As we pointed out in our February report, “Traders and speculators priced out of the gold market flock to silver in precious metal bull markets, driving up volatility and price. The silver market is not as liquid as the gold market, making sudden increases in investment demand responsible for outsized effects. Because of this, silver has a history of outperforming in precious metal bull markets and underperforming in bear markets.”

Silver shines when the focus on it shifts to speculation and it becomes a financial metal. As the chart above illustrates, this can happen overnight, often spurred by rallies in gold. Silver’s split personality helps to explain why it took so long to break out of its 4-year trading range while gold kept making new, all-time highs.

High Interest Rates Hurt Silver More than Gold

Holding physical silver has a built-in opportunity cost. Silver pays no interest. A buyer of silver forgoes the amount of interest he or she could make in risk-free investments like CDs or government securities. This is known as an “opportunity cost.” These opportunity costs climb as interest rates rise. An investor holding $100,000 in silver forgoes approximately $5,000 that he or she could make by purchasing a 12-month FDIC-backed CD yielding 5.0%. This doesn’t include the actual costs of owning physical silver – like shipping, storage, dealer markup and insurance.

The same holds true for gold. However, there are extremely liquid proxies to physical gold, such as ETFs and mining stocks. Some gold stocks even pay dividends. Alternatives exist for silver too, but like the metal itself, are not as liquid. Gold is cheaper to ship and store than an equivalent dollar value of silver due to its sharply-higher price per ounce. Gold nearly always trades like a financial metal. It also benefits from central bank demand. This discourages individual investors from making big investments in silver, especially when high interest rates impose a large opportunity cost upfront.

Currently at 3.27%, inflation is down sharply from its high of 9%, putting Jerome Powell and Company on a glide path towards their 2% target. The latest Fed meeting may have disappointed those who expected rate cuts sooner, but it did confirm the next move will likely be a cut. We believe silver will be far more attractive once the market perceives the Fed is serious about reducing interest rates – and begins reducing them. Silver soared even with the opportunity cost of high, risk-free rates and without a single rate cut yet this year. Imagine what it could do with them.

Gold Still Leading, But Silver is Catching Up

Why look at silver if gold is the metal making new highs? Because silver has a long history of catching up and outperforming gold in bona fide bull markets. Gold continued to make new all-time highs once it powered through the key $2,152 per ounce level we identified in our February report. It gained 14% before stalling out twice around the $2,450 level. Silver rallied 34% during the same period, outperforming its richer cousin 2.4 to 1. We expect silver to do better this time around as well.

Global silver demand is expected to reach 1.2 billion ounces in 2024, the second highest ever according to the Silver Institute. Much of this increase is from stronger industrial demand – especially from photovoltaic (solar panel) and automobile industries. High industrial demand is expected to keep silver in a deficit in 2024, with demand outpacing supply by 176 million ounces.

The potential for conflict surrounding the November election could also be a factor. As we wrote in our February report, “The country is sharply divided and extremely mistrustful of the other side. The election is close. A narrow victory by either candidate runs the risk of being rejected by the opposition as illegitimate. Protests, massive demonstrations and even violence are possible. It hurts us to even imagine this possibility, but it cannot be discounted given the current environment.”

Things could get nastier than expected and stay that way longer than expected. We would not be surprised to see Russia and China take advantage of any prolonged domestic conflict in America to further their own agendas, including an attack on Taiwan and/or a resumption of armed conflict in Korea. We expect gold and silver to do well as the demand for flight-to-safety grows.

Our New Target is $39 Per Ounce

Our February 2024 price target for silver was the top of its 4-year trading range at $30 per ounce. We also anticipated that, “An extended breakout above this range could set the stage for a run to $40 per ounce.” We got that breakout, but without much follow-through yet. Prices have retreated a Fibonacci-perfect 61.8% to the original breakout point, providing us with an opportunity to re-establish long positions. Our new target is $39.00 per ounce. Multiple closes below $26.25 will negate our bullish outlook.

Use COMEX Call Options to “Rent” Silver for Pennies-on-the Dollar

This strategy is designed to give RMB trading customers upside exposure to silver for a lower cost and risk than purchasing the metal outright – while freeing up capital to generate a return elsewhere. Our strategy also insulates holders from the type of volatility that forced many bulls out of the post-Covid silver market where prices fell hard before taking off in pursuit of gold. (See chart on Page 1.)

We’ll use 5,000-ounce COMEX silver options to create our “pennies on the dollar” strategy. Each option covers 5,000 ounces of silver, making each $1.00 per ounce move worth $5,000 and each 1-cent per ounce move worth $50. Buyers of silver call options pay money, known as a “premium,” for the right but not the obligation to be long silver futures at a specific price for a specific period.

Call option buyers do not buy the market; they merely buy the right but not the obligation to be long that market. The key phrase is “but not the obligation.” Should silver decline or fail to rally before the option expires, the option buyer will simply not exercise the right to buy the futures contract. A silver call option buyer risks the premium paid, plus any transaction costs, nothing more.

Silver call option sellers receive money in exchange for the obligation to sell silver futures at a specific price for a certain timeframe. (Note how this definition is the exact opposite of call option buyers.) Think of it this way: if you are an employer, you pay money to your employees. This gives you the right to tell them what to do. As an employee, you receive money from your employer, obligating you to do what your employer tells you. Options work the same way.

Combine Long and Short Positions to Reduce Risk

We can lower the cost and risk of our bullish position by combining long silver options with short silver options. Our upside target for silver is $39.00 per ounce. We want to position ourselves to capitalize on the recent breakout over silver’s key resistance level of $30 per ounce without a lot of undue risk.

One way we can do this is by purchasing March 2025 Comex silver call options with a strike price of $36.00 per ounce, while simultaneously selling an equal number of March 2025 Comex silver call options with a strike price of $39.00 per ounce. This “bull call spread” pairs the right to buy 5,000 ounces of silver at $36 per ounce with the obligation to sell 5,000 ounces of silver at $39 per ounce.

This spread costs $2,750 as of the close on July 5, 2024, when spot silver was trading for $31.50 per ounce. Compare this to the roughly $157,500 it would have cost to buy 5,000 ounces of silver outright. March 2025 COMEX silver options expire on February 25, 2025. This gives us time for the trade to work, keeping us long through the American election and its aftermath. Should silver fail to trade above $36.00 per ounce on this date, we will lose the entire amount we paid for this spread plus any transaction cost, but no more.

Selling the $39.00 call obligates us to sell silver at $39.00 per ounce, so we cannot participate in any rally above this level. This means the most our bull call spread will be worth is the $3.00 per ounce difference between the two strike prices. Multiply $3.00 times the 5,000-ounce contract size, and you get $15,000 – not a bad outcome given our $2,750 (plus transaction cost) risk.

Note: Prices can and will change, so contact your RMB Group broker for the latest. Your broker will work with you to match a strategy to your risk tolerance and market conditions.

Take Advantage of High Rates and Create Your Own “Silver-Backed” CD

Yields on T-bills and CDs are still high. This makes it possible for silver buyers to lower risk by creating their own “silver-backed” CD. Combine the bull spread strategy above with the purchase of a one-year CD and use the interest to fully offset the cost of your bull spreads.

Comex 5,000 oz. spot silver futures are trading for $31.50 per ounce as we write this, making each contract worth $157,500. Instead of buying 5,000 ounces of silver bullion or a futures contract, you could purchase a 6-month, FDIC-insured CD. (A quick search of www.bankrate.com lists numerous 4 and 5-star FDIC-insured CDs with APYs of 5.00% or higher.)

Subtract the $2,750 cost of our bull call spread from the $157,500 cost of 5,000 ounces of silver and use the $154,750 difference to buy a CD yielding 5.50%. Simple interest on your 6-month CD works out to roughly $3.868. This more than covers the $2,750 cost of a bull call spread. You get both the benefits of today’s higher rates and upside exposure to the silver market.

Please be advised that you need a futures account to trade the options in this report. The RMB Group has been helping clients trade futures and options since 1991 and are very familiar with all kinds of option strategies. Call us toll-free at 800-345-7026 or 312-373-4970 (direct) for more information and/or to open a trading account. Or visit our website at www.rmbgroup.com.

* * * * * * * *

The RMB Group

222 South Riverside Plaza, Suite 1200, Chicago, IL 60606

This material has been prepared by a sales or trading employee or agent of R.J. O’Brien & Associates (“RJO”)/RMB Group and is, or is in the nature of, a solicitation. This material is not a research report prepared by a Research Department. By accepting this communication, you agree that you are an experienced user of the futures markets, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions.

DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION.

The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from trades and statistical services and other sources that RJO/RMB believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades.