In Part A of our “Managed Futures 101” blog post we tried to shed light on this little-known asset class by comparing it to more well-known investments like mutual funds and ETFs. In Part B we’ll delve a little deeper and examine the evolution of managed futures accounts – especially given the exponential growth in computing power, data storage and artificial intelligence (AI).

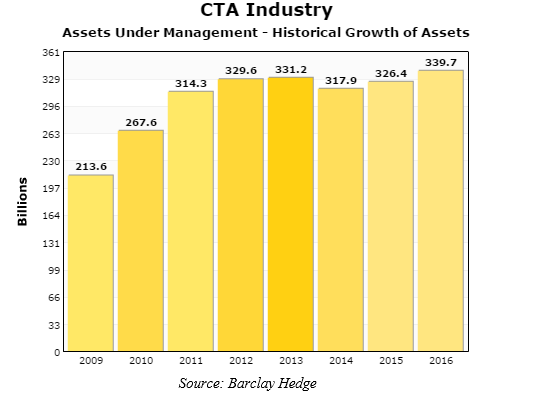

As we outlined in Part A, the Commodity Trading Advisors (CTAs) who direct trading in managed futures accounts trade multiple markets, including but not limited to stocks and bonds. They can also “go short” any of these markets. The combination of these two factors means that the overall performance of managed futures is not linked to the performance of stocks and bonds. This “non-correlation” makes managed futures extremely powerful tools for portfolio diversification. It’s why they continue to grow despite an 8-year bull market in stocks.

Managed futures’ non-correlation gives each CTA the ability to capitalize on both bull and bear moves across a whole series of markets. The incredible growth of managed futures means investors looking for portfolio diversification have many CTAs to choose from. CTAs are highly regulated and tend to concentrate their trading in liquid, open markets. Unlike many hedge funds, most CTA-directed managed futures programs are completely transparent and marked to the market daily. This means no Bernie Madoff-like surprises. It also means most programs offer immediate redemptions with no lock-up periods.

Managed futures investors get a statement every time a trade is made. This is part of the transparency this asset class offers. But complete transparency can be a double-edged sword. Not every trade a CTA makes is going to be a winner. In fact, many of the best-performing CTAs log more losers than winners, but wind up ahead because they keep their losses small in relation to their winning trades.

Getting a series of statements showing consecutive losses can panic investors, causing them to question their commitment to a successful program and exit at the worst moment. Similarly, receiving a series of statements showing gains can generate overconfidence, causing investors to add to programs at inopportune times. Rule of thumb: the best time to add capital to a proven program is during a drawdown – not after a big gain. This is why it is important for investors not to get too hung up on the day-to-day ups and downs of the program(s) they have chosen.

The Evolution of Managed Futures Trading Systems

CTA-directed managed futures programs began to gain popularity in the late 1970s when nearly all trading was conducted in “pits” or “rings” on trading floors. First generation CTAs tended to be “discretionary”, relying on their floor-trading expertise to make buy and sell decisions for their customers. These CTAs tended to focus mainly on their knowledge of individual (mostly agricultural) markets – using their contacts in the industries to gain a trading edge. While there are still some around, they are now the exception rather than the rule.

The advent of computers in the mid-1980s made in-depth technical analysis of individual markets much easier. Systems could be back-tested and modified. This led to the rise of the “systematic” trader. Systematic traders used signals generated by movements in the underlying markets to generate buy and sell signals. These signals enabled the trader to eliminate emotion from trading decisions.

Purely systematic traders don’t pay attention to underlying market fundamentals. Their systems make decisions for them. Limited computing power and data storage meant most of the systems developed in the mid-1980s were “simple” compared with those today. Moving average and trend-following breakout systems were in vogue. Many of these systems required access to company mainframes, putting them out of the reach of individual investors.

Many famous traders (such as John Henry and Paul Tudor Jones) got their starts during this time frame. Some still trade today. Their account minimums are too high for most individual investors now (more on this later), but they’ve adapted to today’s cyber-reality and continue to have success.

Here is a brief outline of how systematic trading systems evolved:

-

- Old School – simple moving average, trend-following, breakout systems mostly using traditional agricultural commodity markets. The time frame of these systems tended to be much longer than many systems today.

-

- Next Gen – increased computing power and data storage allowed for more modeling. Traders were able to test more systems across many markets and custom-fit these systems to the individual price patterns of each of the markets they were interested in. Systems diverged from simple trend-following. Trend-fading, mean reversion and momentum models were added to the mix and custom-matched to individual markets.

-

- System of Systems – the exponential rise of computing power allowed multiple models to be run in a single market. Different techniques were applied to each market. The systems actually used would vary depending on the choices made by a master system or the decision of the CTA. For example, if a market was determined to be in a sideways pattern, trend-fading or mean reversion models would be favored over trend-following systems. The opposite would occur if the market was in a trend.

-

- High Speed and AI – this is where systems have evolved to today. High-speed communication lines mean trading times are reduced to microseconds, making it possible to complete hundreds of thousands of transactions in the time it takes to write this sentence. Artificial Intelligence (AI) algorithms learn as they trade, adjusting the systems they use on-the-fly as the price patterns they encounter change.

There are successful CTAs that use all these methods. That’s why it is important to study the Disclosure Documents of all the managed programs you are interested in and carefully evaluate their track records over time. Only then will you have the information you need to make the right choice for you.

Success Often Means Higher Minimums

Unlike mutual funds which can be bought or sold in small dollar amounts, managed futures programs establish minimum account sizes for their participants. These minimums are what the CTA managing a program deems necessary in order to execute their strategy – at least initially. As successful CTAs get more well-known and in higher demand by professional money managers like family offices, pension funds and university endowments, their minimums tend to rise for a simple reason: it is far easier (and cheaper) to administer a single million dollar account than 10 different $100,000 accounts.

The key is finding up-and-coming CTAs while they are in the “sweet spot.” Look for those who’ve had enough time and managed enough money to prove their chops, but before their success gains them the spotlight and puts them out of reach for most individual investors from an account minimum standpoint. This is ultimately what the managed account professionals here at RMB Group search for.

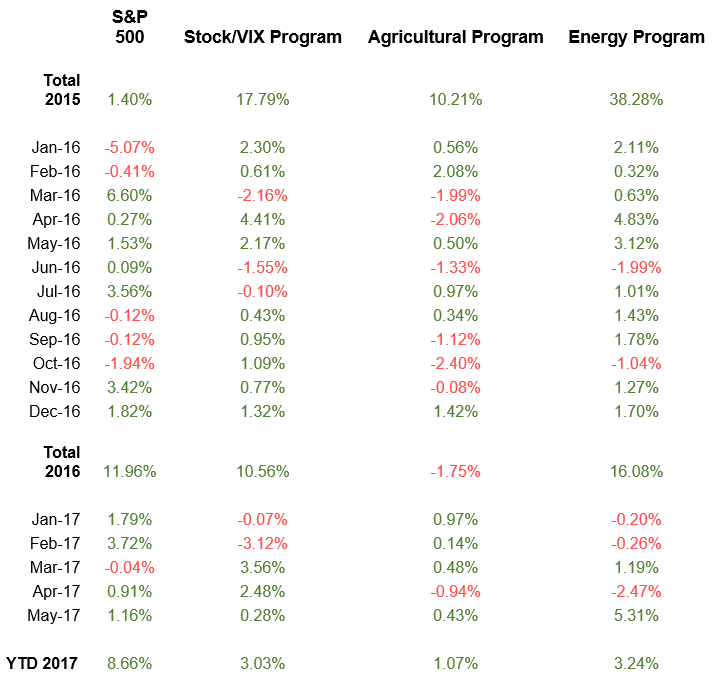

Sample Portfolio Update

We introduced the table below in September 2016. It shows the performance of three Managed Futures programs we are following versus the S&P 500. The first specializes in trading stock market volatility and global stock indexes. The second trades agricultural commodities, and the third focuses on energy. We will update this periodically so our customers have a real-world, dynamic picture of diversification in action.

(Editors’ Note: We have not supplied the name of these programs, because we do not want anyone to enter them based solely on performance shown here.)

Three Managed Futures Programs versus the S&P 500

Investors should consider adding managed futures to their investment portfolios only after carefully reviewing the Disclosure Documents of each CTA they are interested in. A Disclosure Document is to Managed Futures what a prospectus is to stocks. It includes the background, trading style and experience of traders running the program. It also lists risk factors and other information, including the minimum account size each program will accept along with audited track records for the trader(s) running the program(s).

To find out more about the Managed Futures programs the RMB Group is currently following – or to get more information on Managed Futures in general – give us a call toll-free at 800-345-7026 or 312-373-4970 direct. You can also visit our website at www.rmbgroup.com and download our Managed Futures primer “Opportunities Outside the Stock Market” along with a companion video.

—

The RMB Group

222 South Riverside Plaza, Suite 1200, Chicago, IL 60606

This material has been prepared by a sales or trading employee or agent of R.J. O’Brien and is, or is in the nature of, a solicitation. This material is not a research report prepared by R.J. O’Brien’s Research Department. By accepting this communication, you agree that you are an experienced user of the futures markets, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions.

DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION.

The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from trades and statistical services and other sources that R.J. O’Brien believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades.

This report was written by Investors Publishing Services, Inc. (IPS). © Copyright 2016 Investors Publishing Services, Inc. All rights reserved. The opinions contained herein do not necessarily reflect the views of any individual or other organization. Material was gathered from sources believed to be reliable; however no guarantee to its accuracy is made. The editors of this report, separate and apart from their work with IPS, are registered commodity account executives with R.J. O’Brien. R.J. O’Brien neither endorses nor assumes any responsibility for the trading advice contained therein. Privacy policy is available on request.