When do you hold and when do you fold? Nobody can answer this correctly – at least not consistently. The public stayed on the sidelines for most of the 185% rise in the stock market from its 2009 low. However, left with no safe alternative by the Fed’s zero interest rate policy, Mom and Pop investors are pouring money back into the market after pulling it out at precisely the wrong time during the Lehman Crash.

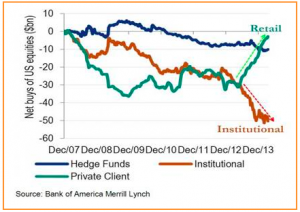

The chart below shows the flow of funds in and out of US stocks by Bank of America customers from 2008 through 2013. “Retail” stock investors didn’t really start buying until last year. Who’s been doing all the selling? “Institutional” investors – also known as the “smart money.”

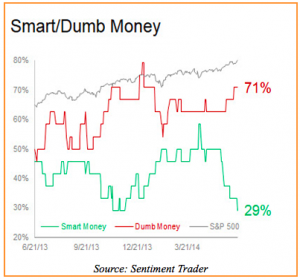

We see this same “smart money” versus “dumb money” dynamic in sentiment surveys. Not only is the “smart money” busy dumping shares, it is far less bullish on the market. 71% of “Mom and Pop” investors are bullish compared with just 29% of the “smart money.”

We see this same “smart money” versus “dumb money” dynamic in sentiment surveys. Not only is the “smart money” busy dumping shares, it is far less bullish on the market. 71% of “Mom and Pop” investors are bullish compared with just 29% of the “smart money.”

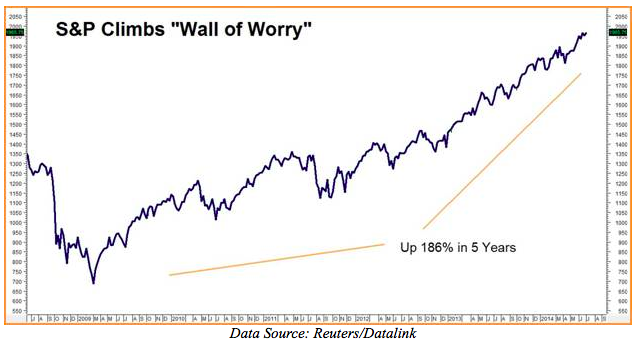

Mom and Pop have been right so far. Stocks have survived and thrived in spite of the near-collapse of Europe, a government shutdown, a rating downgrade of US bonds, countless budget stalemates, a brutal Presidential election, the Russian annexation of Crimea, all-out civil war in the oil rich Mideast – and that’s just for starters! The American stock market ignored it all and became one of the the best global investments of 2012 (up 15%) and 2013 (up 30%). Investors who exited the market based on any of these factors regretted doing so.

There’s a certain level of fear associated with stock market investing. Equities are considered riskier than bonds and other debt instruments that pay investors a fixed rate of return or “coupon.” Bull markets tend to coincide with healthy levels of skepticism, climbing a “wall of worry.” (See second chart below.) The current bull market in stocks is no different. The market could head higher despite worrying extremes in sentiment, valuation and small investor behavior.

One thing is certain. The current rally in stocks will end. When it does, both the odds and human nature favor a severe reaction. Fear is a much more powerful emotion than greed. It clouds judgment and can cause investors to make the worse possible decision at the worst possible time. If the next downturn is anything like previous ones, it will be swift, severe and punishing.

One thing is certain. The current rally in stocks will end. When it does, both the odds and human nature favor a severe reaction. Fear is a much more powerful emotion than greed. It clouds judgment and can cause investors to make the worse possible decision at the worst possible time. If the next downturn is anything like previous ones, it will be swift, severe and punishing.

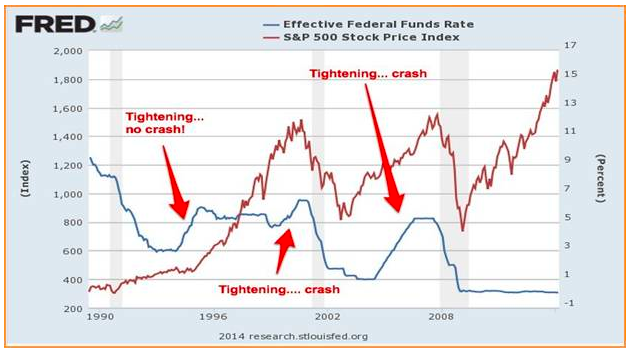

By keeping interest rates artificially low, the Fed and other central bankers are forcing investors into stocks. Confidence has returned, but it is not the healthy belief that the real economy will be better tomorrow. Rather it is the expectation that the Fed or other central bankers will “do whatever it takes” to bail the market out. The second chart (below) shows what happened the last time the Fed took away the punch bowl.

Two of the most important questions we can ask now are: 1) How do we maintain exposure to what has been an incredible run in stocks while guarding against the day when Janet Yellen and Company stop actively supporting stock prices? 2) More importantly, what how do we protect ourselves if and when “whatever it takes” is no longer good enough?

Two of the most important questions we can ask now are: 1) How do we maintain exposure to what has been an incredible run in stocks while guarding against the day when Janet Yellen and Company stop actively supporting stock prices? 2) More importantly, what how do we protect ourselves if and when “whatever it takes” is no longer good enough?

Staying Long But “Hedged”

There are three traditional ways to avoid being burned by a surprise collapse in stocks: 1) sell all or at least a portion of your portfolio; 2) “hedge” your stock positions selling futures contracts or; 3) hedge your portfolio by purchasing put options. Selling your stocks can reduce or eliminate your upside exposure to the market, but you also may incur substantial capital gain taxes in the process.

Selling stock index futures against your portfolio merely locks in a price. Losses in the underlying portfolio may be offset by gains in the futures, but gains in the portfolio can also be offset by losses in the short futures hedge. Buying put option insurance can be very expensive. Put options also expire, requiring the repurchase of more puts with longer life to keep a portfolio hedged. Expenses can add up quickly.

Janet Yellen and the Fed are forcing investors to maintain at least some exposure to stocks if they want any hope of generating a meaningful return in this zero interest rate environment. With the risk of a severe correction increasing by the day, finding a workable hedge that isn’t too expensive and won’t prevent stocks in one’s portfolio from generating a return in good times is even more important.

VIX Futures: A Pure Play on Fear

We believe we have found a hedging vehicle that gives us the best of both worlds: protection when we need it and the ability to participate in a continuation of the bull market. That vehicle is the VIX futures traded on the CBOE.

VIX is the symbol for the Chicago Board Option Exchange (CBOE) Volatility Index. It measures the fear imbedded into options traded on the S&P 500 (SPX) reflecting investors’ 30-day consensus view of the future. S&P 500 puts grant the buyer the right but not the obligation to sell the S&P 500 Index at a fixed price for a limited amount of time.

The more fearful investors are, the more they are willing to pay for put option protection. The more they pay, the higher the market volatility implied in the cost of S&P 500 options. This is what VIX measures.

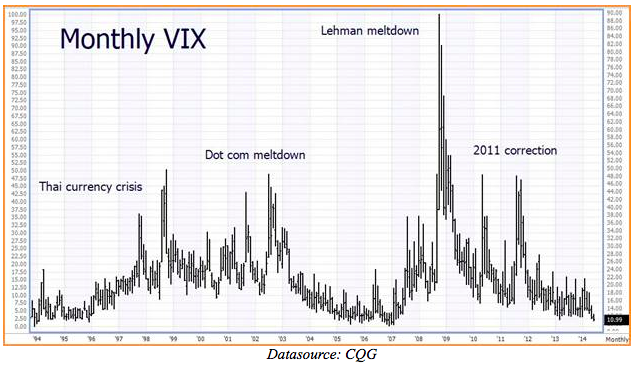

Since fear is the strongest human emotion, it makes sense that VIX would rise and fall in proportion to fear. VIX tends to increase when investors expect big market declines and tends to decrease as fear of those declines subsides. This relationship can be seen clearly in the “Monthly VIX” chart below.

Notice how VIX spikes when confidence in stocks wanes and fear takes over. VIX spiked as high as 90% during the Lehman meltdown which tells you how close to financial Armageddon traders thought we were. Hopefully we won’t see numbers that high ever again.

The most fascinating thing about VIX right now is how low it is – despite all of the potentially game-changing geopolitical factors we listed earlier. VIX dipped below 11% in both June and July 2014. The only time it has been lower was in 2007 when housing was firing on all cylinders. What this means is options traders are so confident in the Federal Reserve’s ability to make things right that they are ignoring the possibilities of a shoot-out between Japan and China, a dangerous miscalculation by Vladimir Putin, or an all-out war pitting Sunni against Shia in the Mideast.

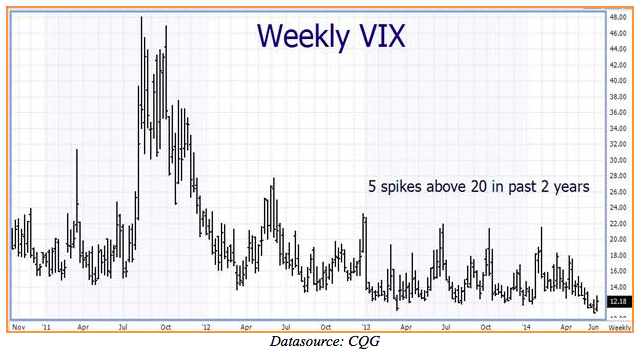

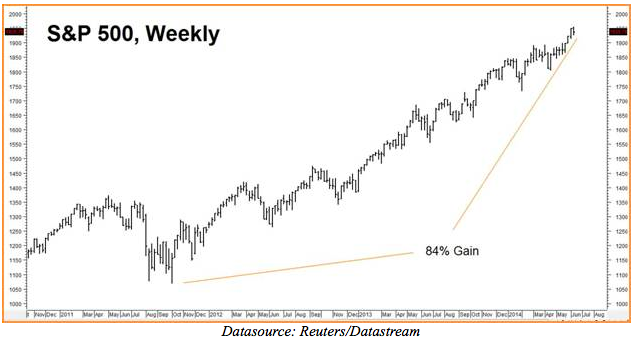

As the monthly chart suggests, stock market confidence can remain high and volatility correspondingly low for extended periods of time. But high confidence and subdued fear do not last forever. The weekly chart (above) shows the history of VIX over the past two years. It has spiked over 20% five times – despite an incredibly strong stock market that gained a remarkable 84% over the same timeframe. Imagine what would happen if the market’s underlying assumptions about the Fed and the “Yellen put” were called into question.

In the two weekly charts above, notice how VIX spikes every time there is a correction of any magnitude, even in a bull trend. It also tends to skyrocket during big downturns such as the ones shown on the monthly chart and on the weekly chart in the spring of 2011.

Unlike selling stocks, shorting futures contracts or buying put options outright, you can use VIX effectively while retaining most of the earning power of your underlying stock portfolio. Unlike these traditional hedging strategies, you are not locking in a low price or paying a fortune in option premium for protection.

Timed right, VIX works as a hedge from any price level because its main driver is fear. Its ability to spike above 20% five times during one of the strongest two-year bull markets in history is testament to that. We asked readers to consider buying VIX as a speculative play or to hedge stock value the last time it dipped below 12% in March 2013. It’s time to do it again.

VIX Futures: The Basics

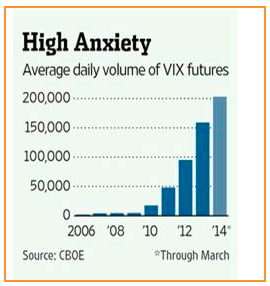

VIX futures trade on Chicago Board Options Exchange (CBOE). The underlying value of VIX futures is $1,000 times the Index. That would make VIX futures at a price of 12.00% (as of the close July 2, 2014) worth $12,000 and VIX futures at a price of 47.00% worth $47,000. VIX is purely an electronic contract. Regular trading hours are 8:30 am to 3:15 pm Central Time. Extended trading hours make VIX tradable nearly 24 hours per day, starting Sunday at 5pm Central Time. Liquidity is excellent because volume is exploding. We are obviously not the only ones using VIX as a hedging tool.

Since volatility cannot drop below zero, buying VIX at 12.00 or lower implies a maximum risk of $12,000 plus transaction cost. Since VIX rarely drops below 9%, a hedging strategy based on buying VIX has a much lower practical risk. If we had purchased VIX futures at the low end of its trading range hedge prior to the 2010 or 2011 corrections, we would have been pretty well-protected.

Since volatility cannot drop below zero, buying VIX at 12.00 or lower implies a maximum risk of $12,000 plus transaction cost. Since VIX rarely drops below 9%, a hedging strategy based on buying VIX has a much lower practical risk. If we had purchased VIX futures at the low end of its trading range hedge prior to the 2010 or 2011 corrections, we would have been pretty well-protected.

Using VIX as a Hedge

Let’s assume that we purchased one VIX futures contract for each $100,000 of stock exposure in our portfolio and paid an average of 17.00% ($17,000) for each contract prior to the 2011 correction. (See “Weekly VIX” chart above.) When the VIX subsequently spiked to 47.00% ($47,000), gains in each futures contract would have offset roughly $30,000 worth of losses (or roughly 30%) in our stock portfolio. Similarly, buying one VIX futures contract for each $200,000 in our portfolio would have offset a loss of roughly 15% in the underlying portfolio. Changing the number of contracts we buy allows us to dial up or dial down our coverage at will.

While there is no guarantee this level of protection will manifest itself in future declines, the charts (above) clearly show a pronounced tendency of VIX to increase sharply during major stock market corrections. Margin to trade one futures contract is currently $3,300.

Buying VIX futures at or below 13.00 and posting $5,000 to cover declines below 8% for each $100,000 to $200,000 in portfolio value looks to be a solid, viable strategy. To make this strategy work properly, you must be committed to your hedge –willing to endure shorter-term losses and roll your position forward as the market dictates. RMB Group trading customers may want to consider calling their personal broker to learn more about implementing this strategy.

Getting Started

You cannot trade VIX futures in your stock account. You need a separate commodity account. The RMB Group has been helping their customers trade futures and options since 1984 and are intimately familiar with the strategy in this report. Contact us or call us toll-free at 800-345-7026 or 312-373-4970 direct. We’ll send you everything you need to get started. Or visit us at www.rmbgroup.com to open an account online.

If you are new to futures and options and would like to know more, give us a call at the phone numbers above or e-mail suerutsen@rmbgroup.com and we will send you the RMB Short Course in Futures and Options (a $14.99 value) absolutely free. You can also download the “Short Course” from our website at www.rmbgroup.com.