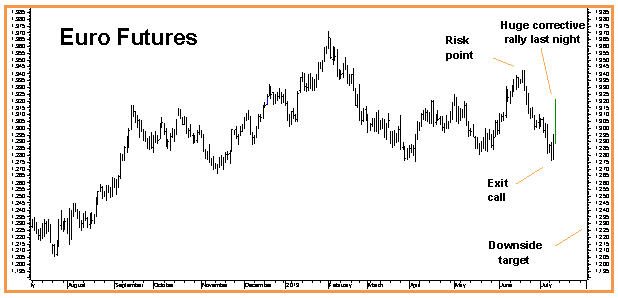

We suggested exiting half of our bearish September put spreads in the euro two days ago because prices were oversold and testing good support. The chart said, “be careful,” and we were. What we did not expect is to see a violent upward correction eliminate the oversold condition in the euro in one big “whoosh” that lasted no more than a couple of hours, and turned every profitable short position entered over the past two weeks into losers overnight – literally.

Welcome to the modern marketplace. Markets often are Bipolar – turning on a dime. This is why we prefer to trade options – not Forex, and certainly not expensive, leveraged currency ETFs. Options give us the staying power to weather a two-day, 5-handle move against our core position in the euro without missing a beat.

What caused the big “melt up” in the euro? Ben Bernanke, of course. Who else would have that kind power? His comments after the North American close yesterday seemed to contradict the more hawkish comments he made in June and suggested, ever-so-slightly, that perhaps the Fed wasn’t in such a big hurry to “taper” its bond buying or to raise short term interest rates sooner than 2015.

That’s all it took. The euro soared from under $1.2900 to over $1.3200 in the blink of an eye.

We don’t believe Gentle Ben’s comments have changed a thing as far as the “taper” or Europe is concerned. The Eurozone remains a basket case in need of a weaker currency. The US economy, bolstered by a red-hot housing market, is not heading for a big slowdown any time soon.

Let’s use this morning’s rally as an opportunity to re-establish the bearish positions we suggested lifting just two days ago. The December bear put spreads suggested below give us three additional months time for less than we sold our September $1.2200 / $1.2600 put spreads for just 2 days ago.

Two consecutively higher closes over old swing highs of $1.340 would negate our bearish outlook for the time being. We’ll consider using this as a signal to exit and limit losses should it occur.