There is a lot of talk in the financial press about abnormally low volatility in stocks. VIX has dropped below 10% numerous times since the Trump rally began. But one of the most surprising factors in 2017 has been the overall lack of market volatility in the commodity markets, even in those commodity markets typically defined by high volatility. As a rule, commodities are more volatile than stocks, but this rule is being tested. Volatility has slipped well below historically low S&P volatility in certain individual commodity markets.

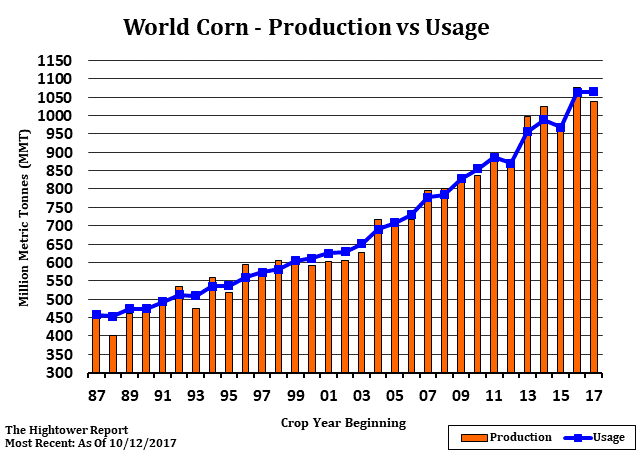

In last week’s Big Move Trade Alert, we identified sugar as one of these markets. This week we are focusing on corn. Like sugar, corn volatility is often dependent on weather. Good growing weather tends to keep a lid on both price and volatility. Five years of near-perfect growing weather in the North America, South America and China have produced bumper crops which have virtually offset rising global demand.

The ability of successive bumper crops to keep pace with growing demand has kept corn prices low, but it has also caused corn option premium sellers to become complacent. Increasing global demand due to increased population and the changing eating habits of heavily-populated China and India requires the need for ever-larger corn crops. This means any reduction in supply due to unexpected weather events such as excessive heat and/or drought has the potential to throw the delicate supply/demand balance that has defined the corn market for the past few years out of whack.

Corn option sellers typically demand a hefty premium to cover the possibility of adverse weather. But not this year…

Corn Options Pricing In No More Than

A 10.3% Move over the Next 34 Weeks…

July corn options expire on June 22, 2018, which is roughly 34 weeks from now. July corn futures are oscillating either side of $3.80 per bushel. The cost of buying both a July $3.80 call (which gives us the right but not the obligation to be long corn at $3.80 per bushel) and a July $3.80 corn put (which gives us the right but not the obligation to be short corn at $3.80 per bushel) is 39 cents ($1,950). 39 cents is 10.3% of the current $3.80 corn price. This means that option traders do not expect corn prices to move more than 10.3% in either direction over the next 241 days (34 weeks).

This makes June 2018 corn implied volatility a full percentage point lower than S&P 500 VIX, which closed yesterday at 11.07%. This is even more astounding when you consider that VIX is calculated with soon-to-expire options. Go further out in time and stock market VIX rises substantially. June 2018 VIX futures are pricing in volatility of 16.25% — nearly 6 percentage points more than the 10.3% currently priced into the June 2018, “at-the-money” corn option straddles.

…And No More Than A 13.9%

Move Over the Next 59 Weeks

Stranger still is the extremely low implied volatility priced in to December 2018 corn options. December 2018 corn futures closed yesterday for $3.98 per bushel. The December 2018 $4.00 call / $4.00 put “straddle” closed for 55 cents ($2,750). 55 cents is 13.9 percent of the roughly $4.00 price for December 2018 corn. This means corn option sellers do not expect a move bigger than 13.9% at any time during the next 12 months.

July corn futures are considered to be “old crop” corn. The price of July corn futures is price is mostly determined by 3 things: 1) existing stockpiles 2) global demand and 3) the South American crop. In the Southern Hemisphere, grain (including corn) is harvested in the North American spring. This means the size of the South American crop is a big factor in the price of July corn futures.

December 2018 futures are called “new crop” futures because their price also factors in the “new” American crop. There are 4 factors at work to determine the price of December corn; the three mentioned for the July futures above plus the state of the North American “new” crop. The US is the world’s biggest corn producer, making the US crop critical to global supply. December 2018 corn options also have 25 more weeks of life than July options, on top of being exposed to a whole new growing season. There is a lot more time for something to go wrong weather-wise.

Mother Nature can be particularly capricious and disruptive – especially in this era of global climate change. As the chart below illustrates, weather can cause corn price and volatility to spike rapidly. History tells us that extended periods of sideways market action tend to resolve to the upside –especially when these periods occur at the lower end of corn’s historical trading range. Prices have been moving sideways for three years now. We do not expect this to last much longer.

This is why we believe 13.9% volatility level currently priced into December 2018 corn options could be just as much of a premium buying opportunity as the 10.3% built into July 2018 corn. Prices have not moved significantly in three years. Corn option traders have priced in a continuation of this sideways movement for another year. But markets do not move sideways forever.

While corn certainly could head lower or continue its sideways drift, we believe the “best of all possible worlds” in terms of global supply is already baked into the market. This increases the odds that any bullish weather surprise will create a rapid and potentially outsized repricing, putting at least 2 of the 12-month price targets shown on the chart below well within reach over the next 12 months.

Data Source: Reuters / Datastream

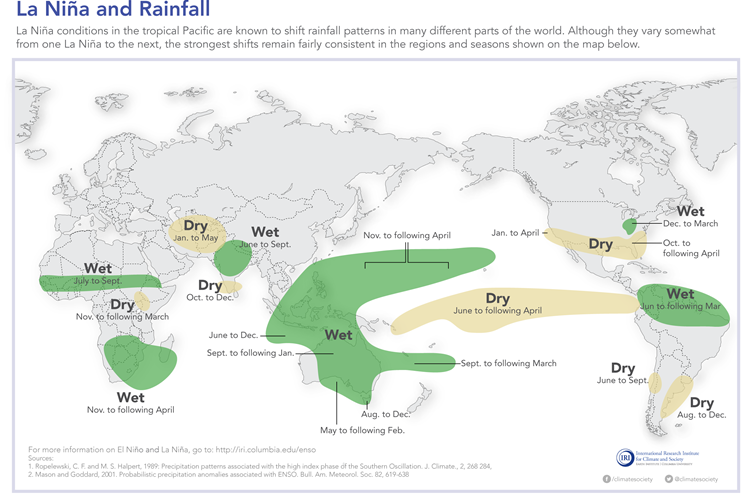

Scientists Forecasting Return of La Niña

What could cause a bullish weather event for corn? La Niña is certainly a possibility. La Niña and El Niño are the nicknames of the two extreme phases of an ocean phenomenon in which water sloshes back and forth across the Pacific Ocean, bringing either warmer-than-normal or colder-than-normal water to the Tropical Eastern Pacific. La Niña’s little brother, “El Niño” is the name used for the warm phase. “La Niña” is the name of the cold one.

La Niña is typically associated with drier-than-normal conditions for key grain producing areas of both North and South America as well as colder-than-normal winter temperatures in the northern US. And while her potential return does not necessarily mean compromised corn supplies in in 2018, inexpensive corn options are presenting investors with a chance to buy some “opportunity insurance” on the cheap.

Options to Consider

The last three bullish breakouts from extended sideways, trading ranges in corn resulted in moves (from low to high) of 99%, 135% and 130% respectively. While we are certainly not forecasting a similar move next year, we do feel fairly confident that any bullish weather surprise should be enough to push corn significantly higher than current levels. The incredible growth in global demand means a continuation of the bumper crops of the past 5 years are essential to price stability. Any disruptive weather event could send prices higher in a hurry.

Our first target of $4.50 per bushel represents an upward move of just 11% in the December 2018 futures contract. Our second objective of $5.20 represents an upward move of 30% and our third objective of $6.40 represents a rally of 60% from current levels.

While all corn options are relatively cheap right now, we believe the best bargains are the “at-the-money” or “close-to-the-money” calls in both the June 2018 and December options. July “at-the-money” calls would need a rally of approximately 20 cents (5.2%) before they became profitable. December “at-the-money” calls would need a rally of 25 cents (6.25%) to achieve the same thing.

July “at-the-money” $3.80 calls closed yesterday for 20 ¾ cents or $1,037.5 each. We believe a price of 20 cents ($1,000) or lower is extremely reasonable. If filled at 20 cents, your maximum risk is $1,000 plus transaction cost. These $3.80 calls would be worth at least $3,500 at our $4.50 per bushel objective, $7,000 at our $5.20 objective, and $13,000 at our $6.40 objective. The market would need to achieve these objectives prior to July option expiration June 22, 2018.

December 2018 “at-the-money” $4.00 corn calls closed yesterday for 26 3/8 cents ($1,318.75). We believe a price of 25 cents ($1,250) or less is extremely reasonable. If filled at 25 cents, your maximum risk is $1,250 plus transaction cost. These calls would be worth at least $2,500 at our $4.50 objective, $6,000 at our $5.20 objective, and $12,000 at our $6.40 objective. December 2018 corn options expire on November 23rd, 2018.

It is possible to lower the cost and risk of these bullish positions in corn by selling more distant call options and using the premium received to help offset the cost. Doing this will make the trade cheaper, but it will also lower the potential for gain. One could also purchase call options further away from the market for less money. These “out-of-the-money” call options are relatively cheap from a historical basis but not as good of a deal — at least in our estimation — as the “at-the-money” calls.

Check with your personal RMB Group broker if you are interested in taking a bullish position in corn. He or she can help you design a strategy to fit both your budget and risk tolerance. Please be advised that you need a futures account to trade the recommendation in this report. The RMB Group has been helping clients trade futures and options since 1984 and are very familiar with all kinds of option strategies. Call us toll-free at 800-345-7026 or 312-373-4970 direct to learn more about this trade.

If you are new to futures and options and simply want to learn more about them, you are welcome to download the RMB Short Course in Futures and Options. This free, easy-to-read guide covers all the basics. Call us toll-free at 800-345-7026 or 312-373-4970 direct for your free hard copy or go to our website at www.rmbgroup.com. Click the “Education Tools” tab at the top of the home page and scroll down to find a downloadable pdf. There is no obligation.

* * * * * * * *

The RMB Group 222 South Riverside Plaza, Suite 1200, Chicago, IL 60606

This material has been prepared by a sales or trading employee or agent of R.J. O’Brien and is, or is in the nature of, a solicitation. This material is not a research report prepared by R.J. O’Brien’s Research Department. By accepting this communication, you agree that you are an experienced user of the futures markets, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions.

DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION.

The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from trades and statistical services and other sources that R.J. O’Brien believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades.

This report was written by Investors Publishing Services, Inc. (IPS). © Copyright 2017 Investors Publishing Services, Inc. All rights reserved. The opinions contained herein do not necessarily reflect the views of any individual or other organization. Material was gathered from sources believed to be reliable; however no guarantee to its accuracy is made. The editors of this report, separate and apart from their work with IPS, are registered commodity account executives with R.J. O’Brien. R.J. O’Brien neither endorses nor assumes any responsibility for the trading advice contained therein. Privacy policy is available on request.