Sometimes patience pays. In early March, we wrote a Special Report on the euro as part of our Investing in Global Chaos series. It has taken a good two months, but the common currency is finally starting to move according to our expectations. Our main thesis was deflation in Europe would force the ECB to take steps to weaken the euro. Deflation is a problem because it increases the real value of current debt. And debt is what Europe has plenty of – with debt-to-GDP ratios in excess of 100% the norm rather than the exception all across the continent.

When Mario Draghi made his now-famous (or infamous depending on your perspective) statement that he would do “Whatever it takes…” to save the European bond market, his biggest concern was soaring interest rates in the peripheral countries of Southern Europe. His de facto guarantee to backstop this debt caused capital to flood into Europe, generating relatively risk free profits for bond investors but also driving up the value of the euro in the process. With interest rates in Spain, Italy, and even Portugal now close to those in the US, this capital flow is slowing.

His bond market issues may be “solved”, but Mario Draghi faces a new, potentially more damaging problem. Economic growth in the Euro zone is nearly nonexistent, slowing to zero across southern Europe and even in France – Europe’s second largest economy. In terms of meaningful growth, Germany is carrying the load for the entire Eurozone. Meanwhile, the bills continue to stack up in the Southern tier. Without growth to provide revenue to service it or inflation to lower the real value of this debt, the crushing weight of it could prove more than the continent can handle.

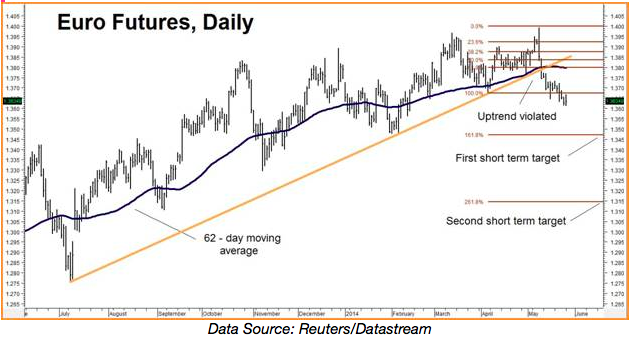

Not surprisingly Mr. Draghi’s focus has shifted to deflation. Without growth, the only way to lower the burden of Europe’s debt is to pay back in cheaper euros. Zero interest rates and negative deposit rates could be right around the corner. Europe needs a weaker Euro. And if we can believe the charts, it’s going to get one. After months of stubbornly testing the high end of its range, the Euro appears to have broken through to the downside – violating its short-term uptrend. Two consecutively lower closes below its old low appear to have confirmed a change in trend. Our short-term Fibonnaci targets are 134.50 and 131.50 on the downside.

The real story however, can be seen on the weekly chart. Prices tested but were unable to take out the long term downtrend line with any kind of significant follow-through. Consequently, our longer-term downside targets of 127.00 and 122.00 remain intact. If you own the September put options we talked about in our March Special Report, continue to hold. If you don’t own put options in the Euro, you may want to consider purchasing some soon.

We are currently recommending an updated bearish put option strategy with a total cost and risk of roughly $1,250 plus transaction costs and the potential to be worth as much as $6,000 should the euro hit our 127.00 objective prior to option expiration in early December. Prices can and do change so RMB trading customers should contact their broker directly for further specifics on this trade. Your broker can also help you custom design a strategy based on your risk level and/or differing price targets.

If you are not an RMB Trading Customer and want to know more about how we are playing this or any other market, contact us give us a call at 800-345-7026 (toll free) or 312-373-4970 (direct) and we’d be happy to go over some of our fixed- risk, “Big Move” strategies with you. You can also e-mail suertusen@rmbgroup.com. Put “Euro” in the subject line.