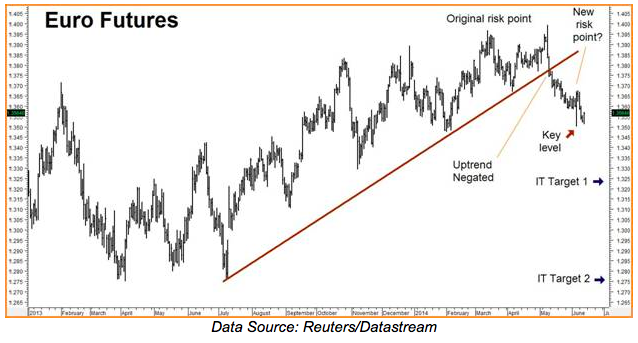

Our recommendation to establish a short position in the euro finally appears to be gaining some traction. The European Central Bank’s (ECB) decision to cut short term interest rates to zero was anticipated by the market and greeted with some skepticism at first. But reality is starting to sink in. The common currency broke below its 11-month uptrend line last month and has been under pressure since. Our intermediate term targets are $1.320 and $1.275 respectively.

We are getting ready to move our risk point down from two consecutively higher closes over $1.3970 in the front contract to two consecutively higher closes over $1.3677. We’ll make this change if the euro closes twice under the $1.3507 low established immediately following the ECB’s rate cut announcement. Taking out this level could break the spirit of the bulls and mark the beginning of a new leg lower.

There are two things the ECB needed to do to stop or at least slow Europe’s slide into deflation: 1) take a page from Ben Bernanke’s playbook and reduce interest rates from .25% to zero and 2) take another page from the same playbook and start buying bonds and injecting cash directly into the system. They completed the first in May, removing the last of the euro’s yield advantages versus the dollar. We expect the second to follow shortly. This could be very euro-negative, especially coming at the same time the Fed is tapering its bond purchases.

If you followed our suggestion to purchase puts and bear put spreads, continue to hold. If you do not have a short position in this market it’s not too late to get one. Call us toll free at the number listed at the end of this report or email suerutsen@rmbgroup.com to request our just updated “Big Move Trade” Special Report: Deflation Fears Say Short the Euro.

Stay Short Japanese Yen

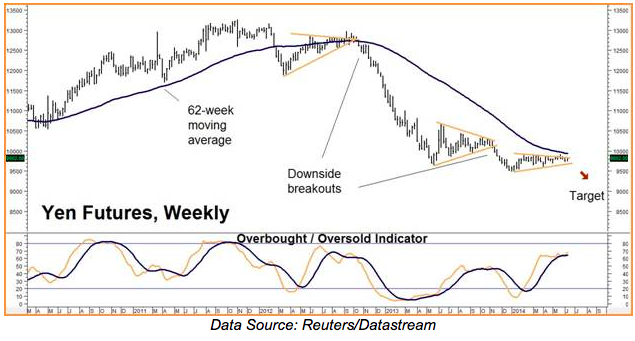

The yen continues to trade in the sideways mode that has defined it for most of the year but we do not think it will last for much longer. The weekly chart appears to be confirming this outlook. The yen has shuffled sideways for the past 6 months, alleviating the oversold condition caused by its previous, breathtaking drop. Price remains below the critical 62-week moving average and after the latest sideways run and appears poised for a third downside breakout. Our target remains .09000 on downside.

It has been a frustrating year so far for the holders of the puts and bear put spreads we’ve been suggesting. But, as the chart above suggests, we don’t think we’ll have to wait much longer to see a substantial move lower. Those without a bearish position in the yen may want to consider taking advantage of this abnormally low volatility to buy relatively inexpensive put options.

Right now we are looking at a strategy with a maximum risk of $900 plus transaction costs with the potential to be worth as much as $6,000 should our first target of .9000 be reached by the beginning of December. Like the euro, we’ve recently updated our “Big Move Trade” Special Report: Japan is an Accident Waiting to Happen. Call us at the numbers listed at the end of this report or email suerutsen@gmail.com to request one.

Aussie Dollar Still Bullish

The Australian dollar is one of the strongest currencies on the board right now. Its ability to rally while nearly every other currency loses value versus the dollar is impressive. Meanwhile, all the technical indicators that convinced us to recommend bullish option strategies remain intact. The Aussie is in a solid uptrend and is holding the key 40-day moving average. Thursday’s new high close for this move was also positive. Our upside target remains .9700 in the front contract.

If you are not an RMB Trading Customer and want to know more about how we are playing this or any other market, contact us give us a call at 800-345-7026 (toll free) or 312-373-4970 (direct) and we’d be happy to go over some of our fixed- risk, “Big Move” strategies with you. You can also e-mail suertusen@rmbgroup.com.