Commodities are just starting to get noticed by the financial press, but a stealth bull market has been raging in this sector for quite some time. Many key markets are up substantially from their lows. The biggest mover is crude oil. It soared from a February 11th low of $26.05 to a May 26th high of $50.21 – an incredible gain of 93%. This kind of move gets everyone’s attention, so it’s no surprise that crude dominated the headlines.

But crude is not the only commodity with a good spring. In our early-May blog post, “Springtime for Commodities,” we explored the budding bull market in all things physical. Now that summer is upon us, let’s take another look. Crude oil was far and away the big winner, but is wasn’t the only commodity that performed well during the first five months of 2016. Corn gained 18%; gold climbed 21%; silver did even better, rising 31%, and soybeans shot up 33%. Sugar was the second best commodity performer, soaring 54% from its 2016 low of 12.45 cents per pound.

These are all BIG moves and RMB has been fortunate enough to be on the right side of several. However, given the sheer number, we need to ask ourselves “just how much gas is left in the commodity tank?” Weather and a topping dollar have provided the fuel so far, but will they continue? Janet Yellen and Company seem to have demurred on a June rate hike and stocks are soaking it in. Will stock market success cause the Fed to change its mind again? The Fed is looking for an excuse to raise rates. A series of new highs in the S&P 500 would certainly qualify.

Most Commodities Aren’t “Cheap” Anymore

Another rate increase could put a temporary damper on some of 2016’s big commodity performers, but we believe commodities have further to run over the long haul. We continue to like our bullish positions in corn, wheat, gold, silver, cotton and sugar – the latter of which is getting very close to our 20 cents per pound. In fact, many of the commodities we follow aren’t “cheap” anymore. Many of these markets are either entering or already in corrective modes. That doesn’t mean the bull market is over. We’ll be looking for entry opportunities to establish or add to bullish positions at lower levels.

There are still three commodities that we consider “cheap” – cotton, coffee and palladium. We have suggested initiating limited risk, long-term long positions in cotton and are taking a good look at coffee. However, there is another way to play the commodity sector that may be the biggest bargain of all – the Australian dollar.

“Backdoor” Play on Commodities

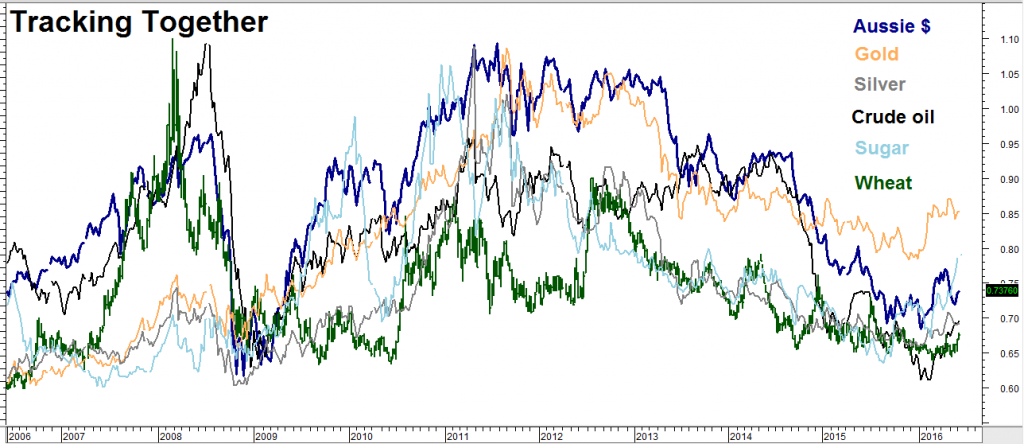

Data Source: Reuters / E-signal

Australia is a major resource producer. Huge exports of copper, iron ore, coal strategic metals, and wheat are just part of what makes the Australian dollar one of the two most liquid “commodity currencies” on the planet. “Tracking Together” (above) illustrates the relationship between the Aussie dollar and some of the commodities in the news recently. While not perfectly correlated, the “Aussie” tends to move with commodities in general, making it an interesting proxy for the entire sector.

Data Source: Reuters / E-signal

As the chart above suggests, the Australian dollar appears to be bottoming. The market has tested and held the key 38-week moving average after its bullish close Friday. This rally confirmed its strength by following through with higher closes on Monday and Tuesday. Unlike crude, gold, silver, soybeans and sugar, the Aussie hasn’t begun a major move higher yet – at least not on a percentage basis. We believe this makes it a relative bargain.

Recent weakness in the Aussie was due to expectations that the Royal Bank of Australia would lower interest rates, making it less competitive with the US dollar. Now it looks like this is not going to happen. At 1.75%, the Australian dollar generates a return 125 basis points higher than the Fed’s .50% return – making the Australian dollar a play on artificially-low US interest rates as well as a “backdoor” play on commodities. Australia’s annual GDP growth of 3.1% is the fastest pace in 3 ½ years – not bad when compared with the roughly 2% growth rate in the US.

RMB Group trading customers may want to consider establishing December bull call spreads using the December CME Australian dollar options. Right now we are looking at a strategy with a maximum risk of approximately $900 plus transaction costs. This could be worth as much as $5,000 if the Aussie reaches our 82-cent objective on or prior to option expiration on December 9, 2016. Consider using a Friday close below the swing low of 71.40 cents as a risk point to exit bullish trades. Your RMB broker may have an alternative way to play this market as well.

If You Are Not an RMB Group Trading Client…

Please be advised that you need a futures account to trade the recommendation in this report. The RMB Group has been helping their customers trade futures and options since 1984 and are very familiar with the strategies suggested in this report. Call us toll-free at 800-345-7026 or 312-373-4970 direct to learn more. We’ll send you everything you need to get started. You can also visit www.rmbgroup.com to open an account online.

If you are new to futures and options and want to learn more, download the RMB Short Course in Futures and Options. This easy-to-read guide covers all the basics. Call us toll-free at 800-345-7026 or 312-373-4970 direct for your free copy or go to our website at www.rmbgroup.com. Click the “Education Tools” tab at the top of the home page, scroll down to find the report.

—

The RMB Group

222 South Riverside Plaza, Suite 1200, Chicago, IL 60606

This material has been prepared by a sales or trading employee or agent of R.J. O’Brien and is, or is in the nature of, a solicitation. This material is not a research report prepared by R.J. O’Brien’s Research Department. By accepting this communication, you agree that you are an experienced user of the futures markets, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions.

DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION.

The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from trades and statistical services and other sources that R.J. O’Brien believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades.

This report was written by Investors Publishing Services, Inc. (IPS). © Copyright 2016 Investors Publishing Services, Inc. All rights reserved. The opinions contained herein do not necessarily reflect the views of any individual or other organization. Material was gathered from sources believed to be reliable; however no guarantee to its accuracy is made. The editors of this report, separate and apart from their work with IPS, are registered commodity account executives with R.J. O’Brien. R.J. O’Brien neither endorses nor assumes any responsibility for the trading advice contained therein. Privacy policy is available on request.